2017年11月10日(金)

観光庁

2017年11月9日

「次世代の観光立国実現に向けた観光財源のあり方検討会」中間とりまとめの公表

~持続可能な質の高い観光立国の実現に向けて~

ttp://www.mlit.go.jp/kankocho/news02_000333.html

次世代の観光立国実現に向けた観光財源のあり方検討会

ttp://www.mlit.go.jp/kankocho/jisedaikentokai.html

中間とりまとめ

ttp://www.mlit.go.jp/common/001209830.pdf

2. 観光財源の確保策について

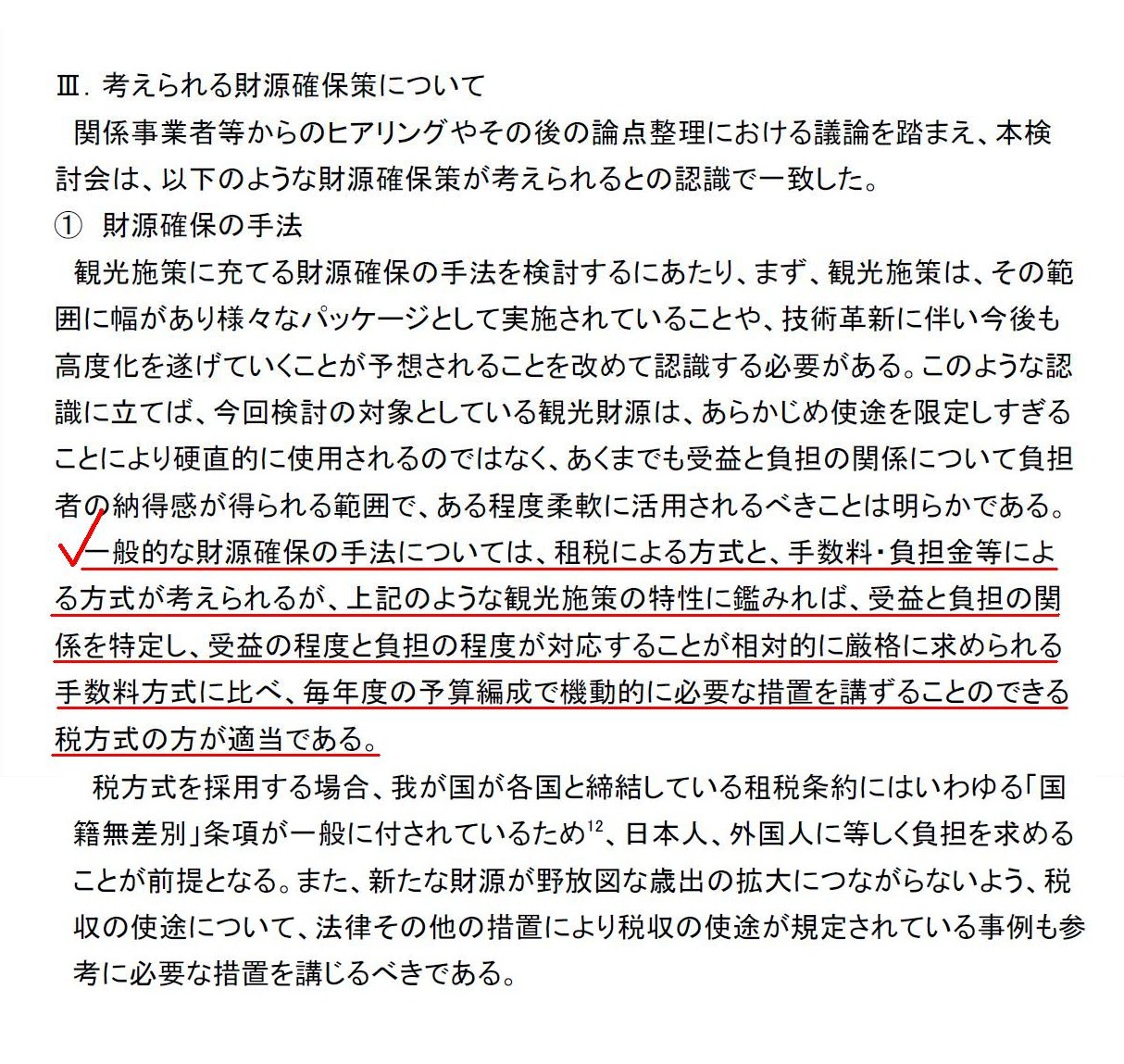

Ⅲ. 考えられる財源確保策について

① 財源確保の手法

(8~9/14ページ)

>一般的な財源確保の手法については、租税による方式と、手数料・負担金等による方式が考えられるが、

>上記のような観光施策の特性に鑑みれば、受益と負担の関係を特定し、受益の程度と負担の程度が対応することが

>厳格に求められる手数料方式に比べ、毎年度の予算編成で機動的に必要な措置を講ずることのできる税方式の方が適当である。

「出国税」に関する過去のコメント

2017年10月30日(月)

http://citizen.nobody.jp/html/201710/20171030.html

2017年10月31日(火)

http://citizen.nobody.jp/html/201710/20171031.html

【コメント】

Originally, financial resources of a country have no concept

"bneficiary payment principle" in them.

When a beneficiary pays what you call

a "charge,"

the beneficiary is burdened with costs of services from which he

benefits to some extent,

whereas, when a beneficiary pays what you call a

"tax,"

the beneficiary is not burdened with costs of services from which he

benefits at all.

The most typical example of the former is a toll of a

superhighway,

and the most typical example of the latter is, as you know, an

income tax.

A toll is sometimes rephrased as a usage tax.

And, an income

tax has no concept "benefit" to a taxpayer in it.

In other words,

conceptually speaking, a "charge" is "one-to-one,"

whereas a "tax" is the

"public benefit."

So, after all, in case that a government has a definite

purpose of some financial resources,

it should collect the resources (i.e.

funds) as a form of a "charge,"

whereas in case that a government has an

indefinte purpose (or general purposes) of some financial resources,

it

should collect the resources (i.e. revenues) as a form of a "tax."

For

example, in case that the gasoline tax is defined as one of the "road specific

resources,"

the gasoline tax is regarded as one of the "funds" for road

constuction

and it should be called a "gasoline usage charge."

whereas, in

case that the gasoline tax is defined as one of the "general resources,"

the

gasoline tax is regarded as one of the "revenues" for general purposes

and it

should be called the gasoline tax as it is.

元来的には、国の財源に「受益者負担の原則」という考え方はありません。

受益者がいわゆる「手数料・負担金」を支払うという場合は、受益者は恩恵を受けたサービスの費用を一定度負担しています。

一方、受益者がいわゆる「税金」を支払うという場合は、受益者は恩恵を受けたサービスの費用を一切負担してはいないのです。

前者の最も典型的な例は高速道路の道路料金であり、後者の最も典型的な例は、御存知、所得税です。

通行料は時に使用税と言い換えられます。

そして、所得税には納税者にとっての「恩恵」という概念はないわけです。

他の言い方をすると、概念的に言えば、「手数料・負担金」は「一対一」であるのに対し、「税金」は「公共の福祉」なのです。

したがって、結局のところ、政府がある財源について明確に限定された用途・目的を持っている場合は、

政府はその財源(すなわち資金)を「手数料・負担金」の形で徴収しなければならない、ということになります。

一方、政府がある財源について明確な用途・目的を持っていない場合(すなわち、全般的な用途に使う場合)は、

政府はその財源(すなわち歳入)を「税金」の形で徴収しなければならない、ということになります。

例えば、揮発油税が「道路特定財源」の1つとして定義される場合は、

揮発油税は道路建設のための「資金」の1つとして見なされますし、揮発油税は「揮発油使用料金」と呼ぶべきなのです。

一方、揮発油税が「一般財源」の1つとして定義される場合は、

揮発油税は全般的な用途のための「税収」の1つとして見なされますし、揮発油税は今のように揮発油税と呼ぶべきなのです。

{kind=link}