2016年7月16日(土)

2016年7月16日(土)日本経済新聞 公告

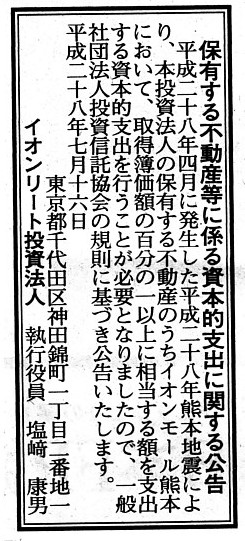

保有する不動産等に係る資本的支出に関する公告

イオンリート投資法人

(記事)

2016年7月15日

イオンリート投資法人

「平成28年熊本地震」の影響に関するお知らせ(第5報)

並びに平成28年7月期(第7期)及び平成29年1月期(第8期)の運用状況の予想及び分配予想の修正に関するお知らせ

ttp://www.aeon-jreit.co.jp/ir/pressrelease/pdf/ARP-9uA6.pdf

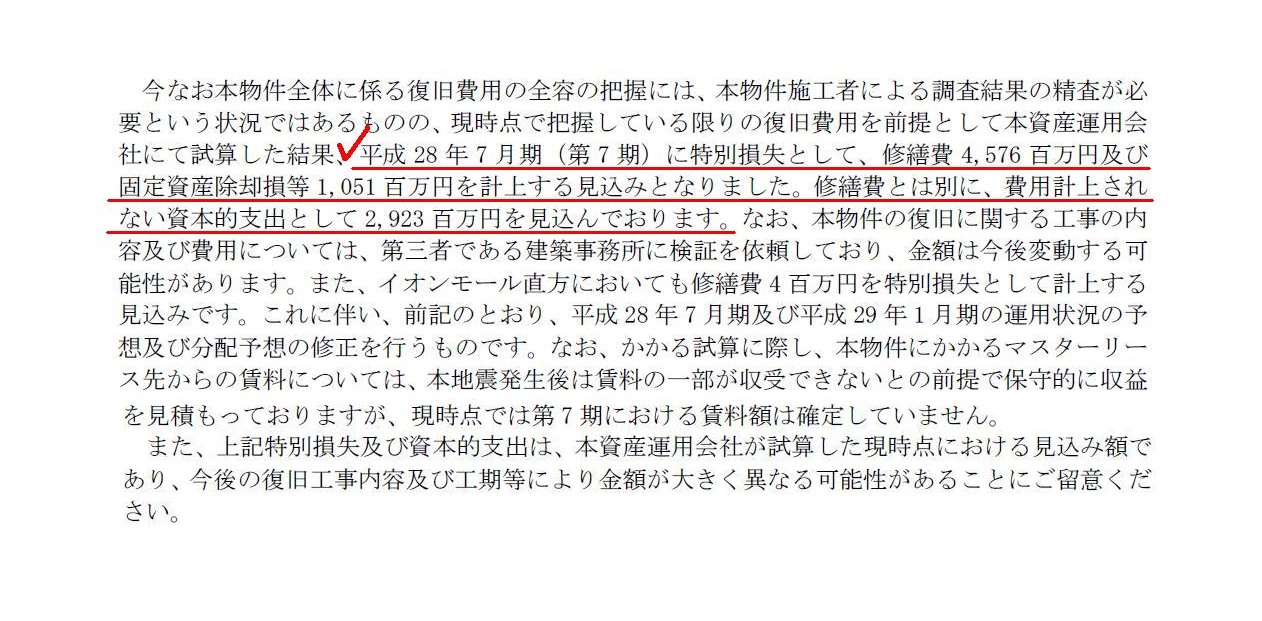

「特別損失の計上」

(2〜3/6ページ)

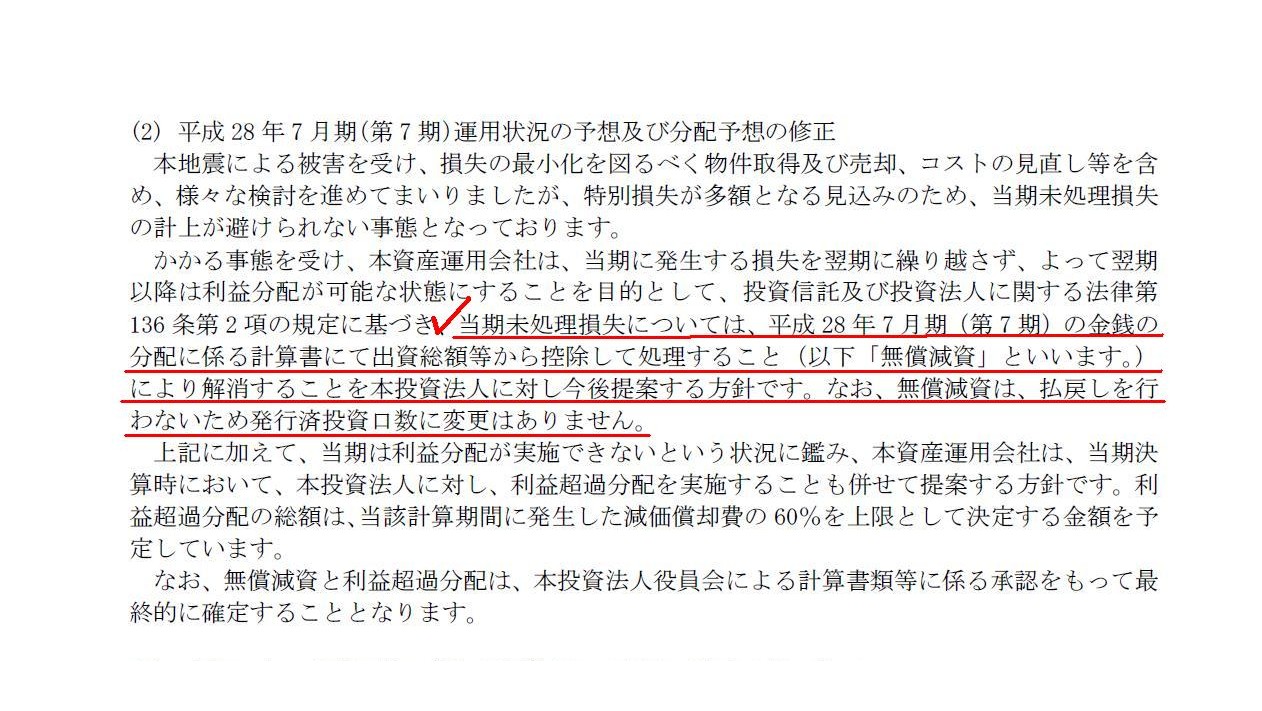

「無償減資」

(3/6ページ)

過去の主な関連コメント

2016年7月14日(木)

http://citizen.nobody.jp/html/201607/20160714.html

2016年7月15日(金)

http://citizen.nobody.jp/html/201607/20160715.html

いわゆる「減資」というのは、文字通り資本取引と損益取引の混同なのです。

From a viewpoint of creditors, a capital expenditure is quite smilar to

an

ordinary cash expenditure on acquisition of an asset.

債権者の立場から見ると、資本的支出というのは通常の資産取得のための現金支出と全く同じなのです。

One idea is that if an ancillary cost is included into an acquisition cost of

an acquired asset,

then a repair cost is also included into an acquisition

cost of a repaired asset.

付随費用を取得資産の取得原価に含めるのならば、修繕費も修繕資産の取得原価に含める、という考え方もあります。

The reason why financial resources of a distribution of a company's assets

are restricted only to profits

is that the company's assets have increased by

the profits.

会社財産の分配の原資は利益のみに制限されている理由は、会社財産がその利益の分だけ増加しているからなのです。

In short, a company distributes "increased assets" only (i.e.

profits).

Ultimately speaking, financial resources of a distribution of a

company are the debit side, actually.

The credit side, or equity, is used

only for calculating the distributable amount.

What you call a "reduction of

a capital" doesn't involve or is not accompanied by an increase in assets of a

company.

So, a distirbution after making a "reduction of a capital" is not,

at least partly, called a ditribution of profits.

簡単に言えば、会社は「増加した財産」のみ(すなわち、利益)を分配するのです。

究極的なことを言えば、会社が行う分配の原資は、実は借方なのです。

貸方、すなわち資本は、分配可能額を計算するために使うだけなのです。

いわゆる「減資」を行っても、会社財産が増加するわけではないのです。

ですので、「減資」を行った後の分配は、少なくとも一部分は、利益の分配とは呼べないのです。

{kind=link}

{kind=link}

{kind=link}