2019年4月8日(日)

2019年4月5日(金)日本経済新聞

郵政、かんぽ生命保険株売却 出資比率65%程度に下げ

(記事)

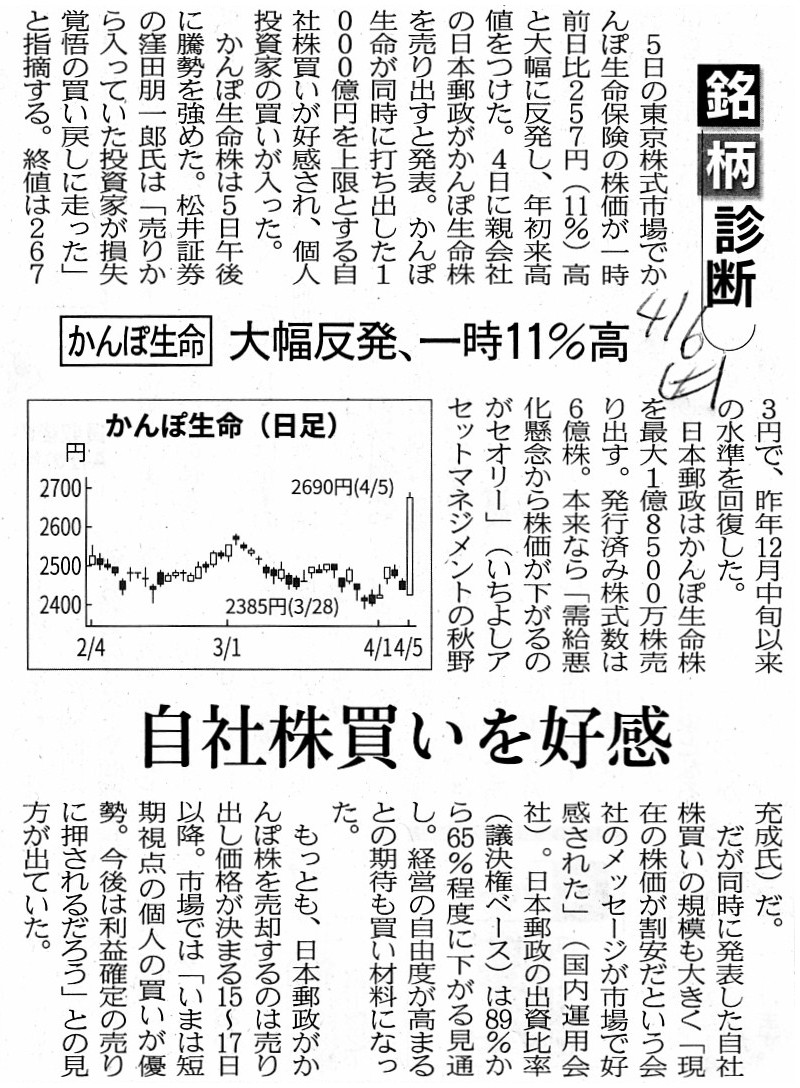

2019年4月6日(土)日本経済新聞

銘柄診断 かんぽ生命

大幅反発、一時11%高 自社株買いを好感

(記事)

2019年4月4日

日本郵政株式会社

連結子会社の普通株式の一部売却に関するお知らせ

ttps://www.japanpost.jp/pressrelease/jpn/20190404_01.pdf

(ウェブサイト上と同じPDFファイル)

2019年4月4日

株式会社かんぽ生命保険

株式売出しに関するお知らせ

ttps://www.jp-life.japanpost.jp/aboutus/press/archives/pdf/20190404pr1.pdf

2019年4月4日

株式会社かんぽ生命保険

自己株式取得に係る事項の決定に関するお知らせ(会社法第459条第1項の規定による定款の定めに基づく自己株式の取得)

ttps://www.jp-life.japanpost.jp/aboutus/press/archives/pdf/20190404pr2.pdf

(ウェブサイト上と同じPDFファイル)

2019年4月8日

株式会社かんぽ生命保険

自己株式立会外買付取引(ToSTNeT-3)による自己株式の取得結果及び取得終了に関するお知らせ

ttps://www.jp-life.japanpost.jp/aboutus/press/archives/pdf/20190408pr1.pdf

(ウェブサイト上と同じPDFファイル)

2019年4月8日

株式会社かんぽ生命保険

売出株式数の変更に関するお知らせ

ttps://www.jp-life.japanpost.jp/aboutus/press/archives/pdf/20190408pr2.pdf

(ウェブサイト上と同じPDFファイル)

2018年12月18日(火)のコメントで、ソフトバンク株式会社の上場に関する記事を計26本紹介し、

「有価証券の上場には4つのパターンがある。」という資料を作成し、以降、集中的に証券制度について考察を行っているのだが、

2018年12月18日(火)から昨日までの各コメントの要約付きのリンクをまとめたページ(昨日現在、合計111日間のコメント)。↓

各コメントの要約付きの過去のリンク(2018年12月18日(火)〜)

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

【コメント】

In practice, under the traditional securities system before

1999,

a "secondary distribution" didn't used to produce any effects on a

share price in the market at all.

実際、1999年以前の伝統的な証券制度では、「売出し」は株式の市場価格に一切影響を及ぼしていませんした。

As at a new listing, a share has no market price yet.

新規上場の時点では、株式にはまだ市場価格はないのです。

Whether inside the market or outside the market, after an investor buys a

share at a price,

he can't complain, "I didin't want to buy the share at the

price."

市場内であろうが市場外であろうが、ある株式をある価格で買った後、

投資家は「私はその株式をその価格で買いたかったわけではありません。」と不平を言うことはできないのです。

Under the traditional securities system before 1999,

a large shareholder

used to be unable to sell his shares inside the market even as at a new

listing.

That is to say, undrer the traditional securities system before

1999,

a large shareholder as at a new listing used to be compelled to sell

his shares through a "secondary distribution."

1999年以前の伝統的な証券制度では、大株主は新規上場時であっても市場内で所有株式を売却することはできませんでした。

すなわち、1999年以前の伝統的な証券制度では、

新規上場時の大株主は所有株式を「売出し」を通じて売却せざるを得ませんでした。

Under the traditional securities system before 1999, extremely

speaking,

there used to exist no concept "supply and demand on a share"

itself in the stock market.

In other words, under the traditional securities

system before 1999,

there used to exist no buy order itself and no sell order

itself in the stock market.

1999年以前の伝統的な証券制度では、極端なことを言えば、株式市場に「株式の需給」という概念それ自体がありませんでした。

他の言い方をすれば、1999年以前の伝統的な証券制度では、株式市場には、

買い注文それ自体がそして売り注文それ自体がありませんでした。

1999年以前の伝統的な証券制度では、株式の需給に応じて株式の市場価格が変動するというのはおかしな考え方であったのです。

1999年以前の伝統的な証券制度では、株式市場に存在していたのは、株式の需給ではなく、株式の取引の相手方だけだったのです。

A "secondary distribution" excludes an effect of a supply and demand on a share from the stock market.

「売出し」は株式市場から株式の需給の影響を排除するのです。

Figuratively speaking,

a share price in the market under the traditional

securities system before 1999 used to be the "given,"

whereas that under the

current securities system is a "result" of a trading of the share.

比喩的に言えば、1999年以前の伝統的な証券制度における株式の市場価格というのは「所与」のものであったのですが、

現行の証券制度における株式の市場価格というのは株式の取引の「結果」なのです。

Let's assume that Aflac Incorporated was listed in Japan of the traditional

securities system before 1999.

When its share price in the market

fluctuated,

an investor holding a Aflac Incorporated share probably said, "Uh

fluctuated."

Under the current securities system, when its share price in the

market fluctuates,

an investor holding a Aflac Incorporated share says, "A

flow of a supply and demand on the share."

アフラック社が1999年以前の伝統的な証券制度であった日本で上場をしていたと仮定しましょう。

アフラック株式の市場価格が変動した時、アフラック株式を保有していた投資家はきっとこう言ったことでしょう。

「あ、変動した。」と。

現行の証券制度では、アフラック株式の市場価格が変動した時、アフラック株式を保有している投資家はこう言います。

「株式の需給の変動だ。」と。

{kind=link}

{kind=link}