2019年3月17日(日)

2019年3月16日(土)日本経済新聞

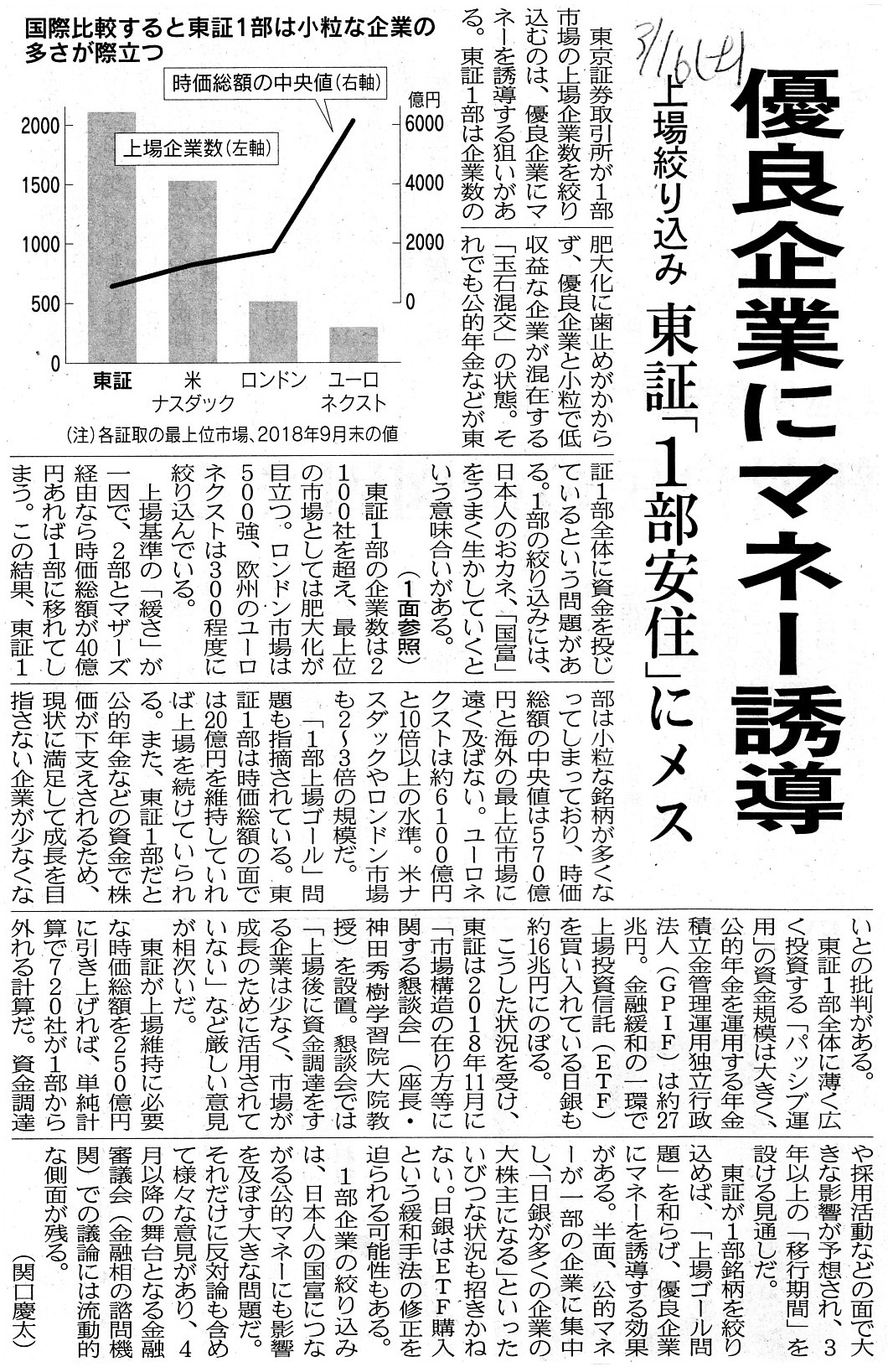

優良企業にマネー誘導 上場絞り込み 東証「1部安住」にメス

(記事)

2019年3月14日(木)日本経済新聞

JPX・東商取、月内にも統合合意 総合取引所 投資に弾み 利便性高め 世界と競争

デリバティブ

成長の要 日本勢、アジアでも出遅れ

東商取、「エネ市場」めざす 電力先物と一体で取引

東商取、独立志向で議論足踏み 3期連続の赤字

構想進む契機に

(記事)

2019年3月11日(月)日本経済新聞

1部上場「緩さ」浮き彫り 2部・マザーズ経由が7割超 東証、今月中に改善案

世界比較でも「甘め」 廃止基準の見直し案も

(記事)

2019年2月27日(水)日本経済新聞

貴金属や農産品 大阪に取引移管 日本取引所・東商取が合意 先物と一体運営 エネ商品焦点に

(記事)

第13章 証券市場のインフラストラクチャー

1. 金融商品取引所

(4) 金融商品取引所の自主規制

(5)

外国金融商品取引所

(6) 「プロ向け」市場

(7) 総合取引所

「344〜345ページ」

2018年12月18日(火)のコメントで、ソフトバンク株式会社の上場に関する記事を計26本紹介し、

「有価証券の上場には4つのパターンがある。」という資料を作成し、以降、集中的に証券制度について考察を行っているのだが、

2018年12月18日(火)から昨日までの各コメントの要約付きのリンクをまとめたページ(昨日現在、合計89日間のコメント)。↓

各コメントの要約付きの過去のリンク(2018年12月18日(火)〜)

http://citizen.nobody.jp/html/201902/PastLinksWithASummaryOfEachComment.html

The "Financial Instruments and Exchange Act" is one of the laws and

ordinances,

whereas "securities listing regulations" of a stock

exchange are one of the self-regulations.

「金融商品取引法」は法令の1つですが、証券取引所の「有価証券上場規程」は自主規制の1つなのです。

A "Foreign Financial Instruments Exchange" prescribed in the Financial

Instruments and Exchange Act is,

figuratively speaking, an exchange version

of the "Foreign Stocks" division set up at Tokyo Stock Exchange.

金融商品取引法に規定のある「外国金融商品取引所」というのは、例えて言うならば、

東京証券取引所に設けられている「外国株」区分の証券取引所版のことなのです。

Merely fiddling about with the machinery of stock markets reminds me of

that "TOKYO PRO Market."

興味本位に株式市場の機構をいじっているのを見ると、私はあの「TOKYO PRO Market」を思い出します。

Investors in the market are neither professional nor amateur.

But, a

stock market has several correct concepts in it.

I want to propose a new plan

stated below.

One stock market is the one with "sell" only and the other

stock market with both "sell" and "hold."

Metaphorically speaking in U.S.,

the former is the "IBM-type" and the latter is the "Microsoft-type."

市場の投資家にプロも素人もありません。

しかし、株式市場には正解が複数あるのです。

私は下記の計画を提案したいと思います。

一方の株式市場は「売却する」だけがある株式市場であり、

他方の株式市場は「売却する」と「保有する」の両方がある株式市場です。

米国で比喩的に言うならば、前者の株式市場は「IBM型」であり後者の株式市場は「Microsoft型」です。

Until now, I have been understanding that, as an object of a trading,

a

share traded in a stock market such as Tokyo Stock Exchange is fundamentally

different

from a commodity traded in a commodity market such as Tokyo

Commodity Exchange.

Actually, I have once written a comment to such

effect.

In short, an object is actually transfered in the former

market,

whereas an object is actually not transferred in the latter

market.

On the contrary, today, I hit upon a new understanding.

To put it

simply, the former market is, in the final analysis, very similar to the latter

market.

For, quite contrary to the original exchange in 1893,

at least in

theory (i.e. at least in the traditional securities system of the modern

times),

investors in the market buy shares merely in order to sell

them

because an issuer doesn't fix the date for its liquidation.

Extremely

speaking, in the modern times,

the intrinsic value of a share is a potential

sell value rather than a liquidation value.

A dividend received annually and

a voting right to be exercised at a meeting of shareholders

are left out of

consideration for reasons of its own, though.

To put it from the other way

around, quite contrary to the traditional securities system before 1999,

some

investors don't buy shares merely in order to sell them in the stock market

after 1999.

Particularly, institutional investors like activist funds buy

shares in the market in order to hold them.

The purpose of their holding

those shares is holding a conversation with an issuer

amicably or out of a

meeting of shareholders.

In Japan, for certain investors, the purpose of

buying shares has converted from "sell" to "hold" exactly in 1999.

The

discussion stated above is truly a fair and netural opinion - I am a man of that

kidney.

今まで私は、取引の目的物として、東京証券取引所のような株式市場で取引される株式は

東京商品取引所のような商品取引所で取引される商品と本質的に異なるものであるとずっと理解をしていました。

実際に、その趣旨のコメントをかつて書いたこともあります。

手短に言えば、前者の市場では目的物は実際に受渡がなされる一方、後者の市場では目的物は実際には受渡はなされないのです。

ところが、今日、私はある新しい理解が頭に思い浮かびました。

簡単に言えば、前者の市場は結局のところは後者の市場と非常に類似しているのです。

というのは、1893年当時の元来の取引所とは正反対に、少なくとも理論上は(少なくとも現代における伝統的な証券制度では)、

市場の投資家はただ売却するためだけに株式を購入するからです。

その理由は、発行者は会社清算の日取りを決めていないからです。

極端なことを言えば、現代では、株式の本源的価値とは清算価値というよりもむしろ売却可能価額のことなのです。

議論の都合上、年1回の受取配当金と株主総会で行使される議決権については度外視していますが。

逆から言えば、1999年以前の伝統的な証券制度とは正反対に、

1999年以降の株式市場では単に売却することを目的に株式を買うというわけではない投資家も中にはいるわけです。

特に、アクティビスト・ファンドのような機関投資家は、保有するために市場で株式を買うのです。

それら機関投資家が株式を保有する目的は、穏便にすなわち株主総会外で、発行者と対話をするためなのです。

日本では、まさに1999年に、一部の投資家にとって、株式を買う目的が「売却する」から「保有する」に変わったのです。

上記の議論は真に公正で中立な意見です――私はそういう人間です。

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}