2018年10月28日(日)

2018年10月24日(水)日本経済新聞

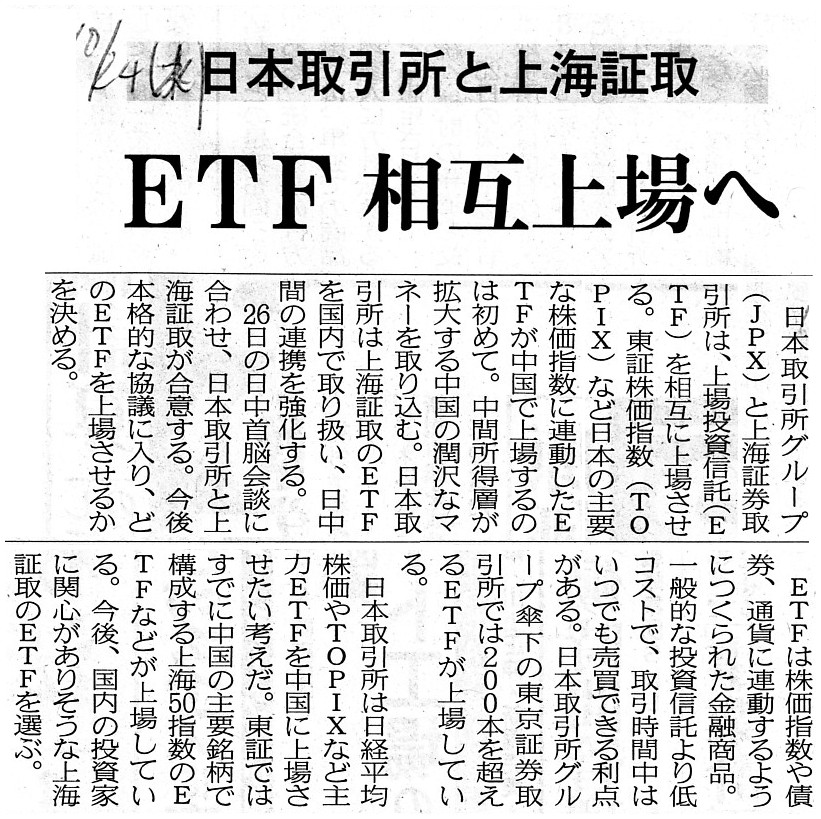

日本取引所と上海証取 ETF 相互上場へ

(記事)

2018年10月24日(水)日本経済新聞

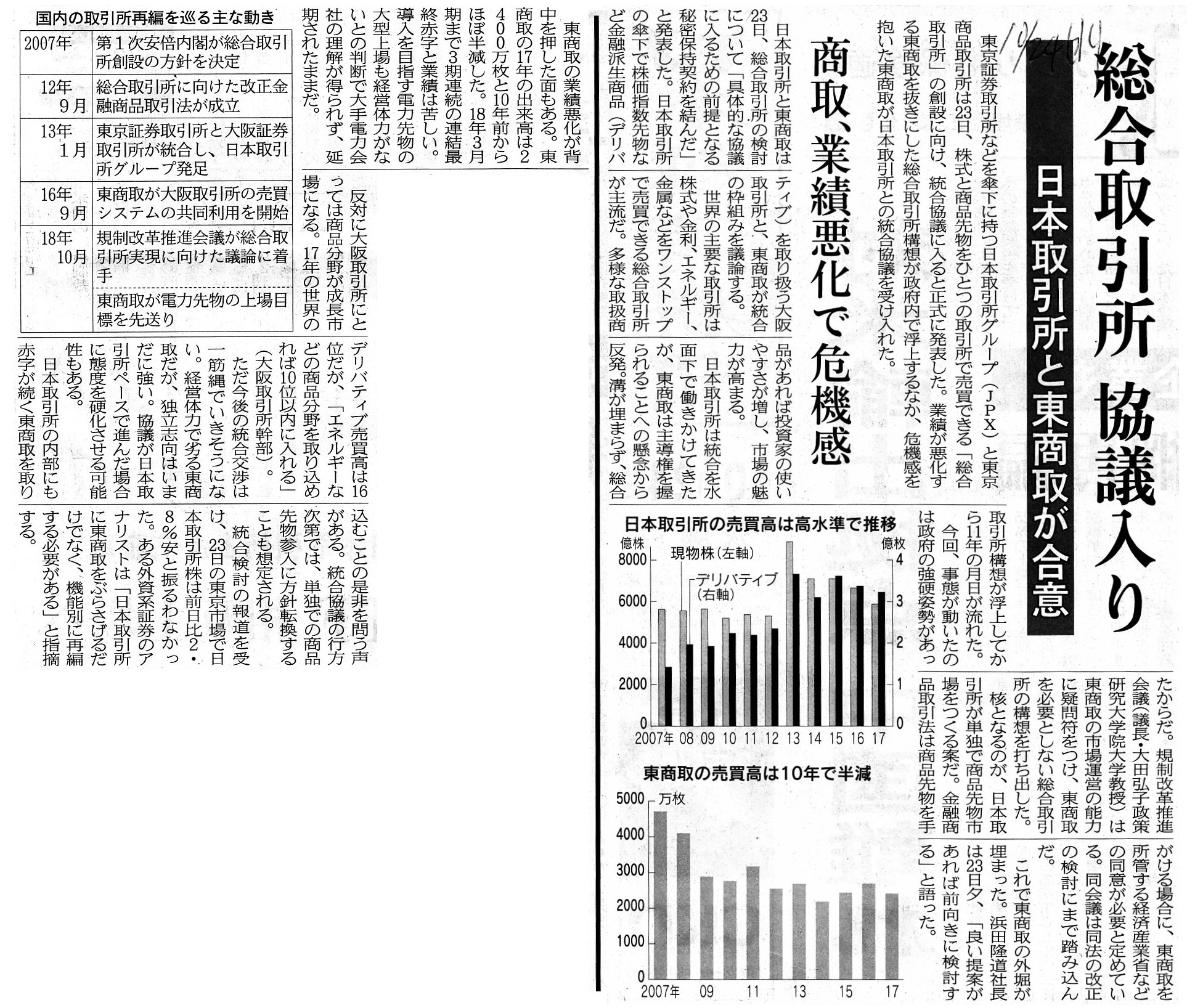

総合取引所 協議入り 日本取引所と東商取が合意 商取、業績悪化で危機感

(記事)

2018年10月25日(木)日本経済新聞

総合取引所へ複数案 日本取引所CEO 枠組みに言及

(記事)

2018年10月27日(土)日本経済新聞 社説

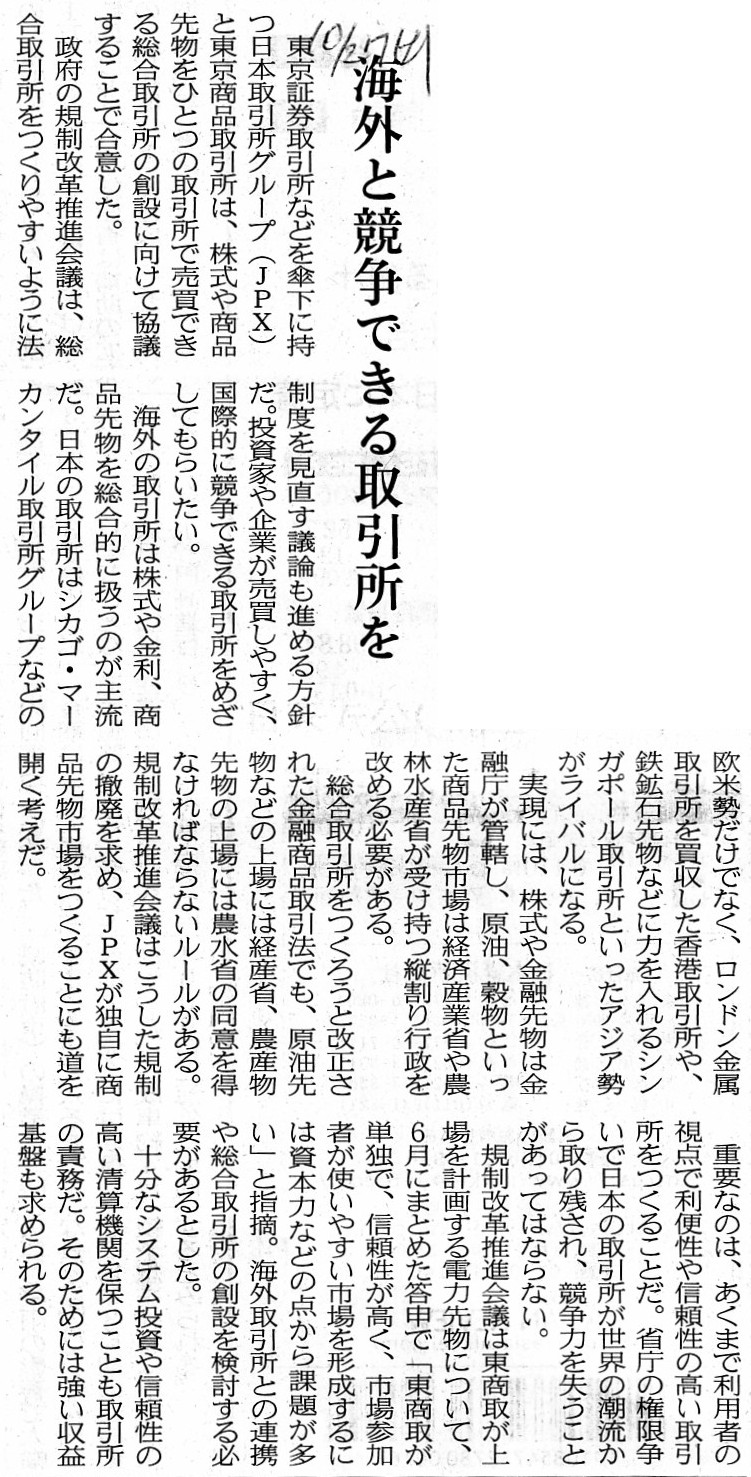

海外と競争できる取引所を

(記事)

「証券取引法が昔は『取引所法』という名称だった理由は、

『投資家は証券取引所で株式の取引を行っていたから』ではなく、『ディスクロージャーにより投資家を保護する。』

という観点・原理から言えば、より本質的には『発行者は証券取引所で情報の開示を行っていたから』なのだと思います。」

と書いた時のコメント↓。

2018年10月22日(月)

http://citizen.nobody.jp/html/201810/20181022.html

>東京証券取引所などを傘下に持つ日本取引所グループと、商品先物を手がける東京商品取引所が統合に向けた検討に入る。

>長年の課題だった株式などの金融商品と商品先物をひとつの取引所で売買できる「総合取引所」の実現へ大きく踏み出す。

>統合すれば、株式からエネルギー、穀物などの商品先物を総合的に取り扱う「総合取引所」が誕生する。

>多様な商品を一つの取引所で売買できるようになるため、投資家の利便性が高まる。

>市場参加者が増えれば流動性が向上し、より機動的な売買が可能になる。

>世界の取引所はデリバティブを成長事業と位置付けている。

>特に重要なのがエネルギーや金属などの商品分野だ。

>世界の取引所ではCMEやニューヨーク証券取引所(NYSE)を傘下にもつインターコンチネンタル取引所(ICE)など

>商品や証券を一体に取り扱う総合取引所が主流だ。

>香港取引所もロンドン金属取引所(LME)を12年に買収し、市場での評価を高めた。

投資家にとっての利便性の向上や関連する法令・法律の改正や所管省庁の整理といった実務上の議論は今日は一切しないことにします。

今日は、株式と商品先物をひとつの取引所で売買できる「総合取引所」という考え方は、

果たして投資家の利益を害するのか否かについて議論をしたいと思います。

「総合取引所」について考察をする時には、2018年10月22日(月)に書きました

概念図「証券の取引に関する全ての活動は、証券取引所内で完結している。」が参考になると思います。

1893年当時は、1つの証券取引所に1つの株式市場しかなかったので、

2018年10月22日(月)に書きました概念図では、証券取引所=株式市場ということを前提にして説明を試みたわけです。

証券取引所内に複数の市場がある場合は、この概念図の「証券取引所」を「市場」という言葉に置き換える必要があるわけです。

では、1つの証券取引所内に異なる目的物を売買できる複数の市場が開設されることは、投資家の利益を害するでしょうか。

この一件に関する第一報は2018年10月23日(火)付けの日本経済新聞の朝刊だったわけですが、

2018年10月23日(火)以来、有事の際の悪影響を始めとして性悪説に立ってこの問題点についてずっと考えてきました。

今日辿り着きました結論は、私には珍しいことに、「『総合取引所』という概念は投資家の利益を害さない。」です。

「市場を運営する取引所は1つだが、目的物を取引する市場は目的物毎に分かれている。」という点が重要な点なのです。

以下、概念図を描きながら私が考察した内容について記したいと思います。

Not only in terms of "trading" but also in terms of "disclosure,"

the

concept "one complex exchange" doesn't harm intersts of

investors.

(「取引」の観点から見ても「情報開示」の観点から見ても、「総合取引所」という概念は投資家の利益を害しません。)

「概念図」

One exchange can set up several markets inside it.

1つの取引所は所内に複数の市場を開設することができます。

There will be several markets in one exchange.

1つの取引所に複数の市場が存在するようになるのです。

Does the fact that one exchange operates plural markets in it harm

interests of investors?

1つの証券取引所が複数の市場を運営することは投資家の利益を害するでしょうか。

At a time, an investor can participate in only one of the markets which

one complex exchange has set up.

投資家は、同時刻に、総合取引所が開設している複数の市場のうちただ1つの市場にしか参加できないのです。

Let's go back to 1893, when the "Exchange Act" was enacted.

And let's

assume that the stock market and the corporate bond market are set up

inside

the Kanto Exchange in the Kanto Local Finance Bureau.

In such case, an issuer

of a stock listed in the stock market submits its legal disclosure

document

to the Kanto Local Finance Bureau and an issuer of a corporate bond

listed in the corporate bond market

submits its legal disclosure document to

the Kanto Local Finance Bureau.

Then, at this point, does the existence of

two markets inside the Kanto Exchange in the Kanto Local Finance Bureau

harm

interests of either investors who trade stocks in the stock market

or

investors who trade corporate bonds in the corporate bond

market?

Interests of neither of them are harmed, I suppose.

For,

conceptually speaking, investors in one market are independent of the other

market.

1893年に戻ってみましょう(「取引所法」は1893年に制定されました)。

そして、株式市場と社債市場が関東財務局の中の関東取引所内に開設されていると仮定しましょう。

そのような場合、株式市場に上場している株式の発行者は法定開示書類を関東財務局に提出しますし、

社債市場に上場している社債の発行者は法定開示書類を関東財務局に提出するわけです。

では、この時、関東財務局の中の関東取引所内に2つの市場が存在することは、

株式市場で株式の取引を行う投資家か社債市場で社債の取引を行う投資家のどちらかの利益を害するでしょうか。

どちらの利益も害されない、と私は思います。

というのは、概念的に言えば、一方の市場にいる投資家は他方の市場からは独立しているからです。

In the modern securities system, conceptually speaking,

all activities

concerning an exchange of securities are completed inside the market.

That is

to say, a set of activities concerning an exchange of securities in one

market

doesn't produce any effects on a set of activities concerning an

exchange of securities in another market.

現在の証券制度では、証券の取引に関する全ての活動は、市場内で完結するのです。

すなわち、ある市場における証券取引に関する一連の活動は、

別の市場における証券取引に関する一連の活動に何らの影響も及ぼさないのです。

From a standpoint of the concept "one complex exchange,"

if the "Exchange

Act" of 1893 is adapted to the modern securities system and the modern

commodities exchange system,

it should be called the "Market Act."

One

market in "one complex exchange" is independent of another market in the

"complex exchange."

「総合取引所」という概念の立場から言えば、

1893年の「取引所法」を現代の証券制度や現代の商品取引制度に即してみると、

「取引所法」は「市場法」と呼ぶべきなのです。

「総合取引所」内のある市場は、同じ「総合取引所」内の別の市場からは独立しているのです。

An issuer discloses information.

Investors trade.

発行者は情報開示する。

投資家は売買する。

When you want to see a movie put on the screen in a cinema complex,

you

can see the movie which you want to see only.

You don't have to see even the

other movies put on the screen in the cinema complex,

シネマコンプレックスで上映されている映画を見たい時は、見たい映画だけを見ればよいわけです。

シネマコンプレックスで上映されている他の映画まで見る必要はないのです。

This is merely my personal opinion, but the concept "one complex exchange"

itself

doesn't run counter to the spirit of the investor protection.

The

reason for it is that the exchange is not the counter party of an

investor

and that an investor doesn't trade an object which is related to the

exchange.

For example, concerning listed securities such as shares and

exchange traded funds,

interests of investors are not harmed as long as an

issuer discloses its information inside "one complex exchange."

And, the

"multiple listing" can't be done inside "one complex exchange"

because kinds

of objects themselves traded in the market are different from each

other.

Therefore, not only in terms of "trading" itself done by

investors

but also in terms of "disclosure" done by an issuer, an miner, a

farmer, a producer and a generator of energy, etc.,

the fact that several

markets exist under one complex exchange doesn't harm interets of investors, I

suppose.

I entirely agree to the concept "one complex exchange" and want to

say, "Leave this unification process alone."

これは私の個人的な意見に過ぎないのですが、「総合取引所」という概念そのものは投資家保護の趣旨に反しないと思います。

その理由は、総合取引所は投資家の取引の相手方ではありませんし、また、

投資家は総合取引所と関連がある目的物を取引するわけでもないからです。

例えば、株式や上場投資信託といった上場有価証券に関して言えば、

発行者は「総合取引所」内で情報を開示しさえすれば投資家の利益は害されないわけです。

また、市場で取引される目的物の種類そのものが異なるので、「総合取引所」内で「重複上場」を行うこともできません。

したがって、投資家が行う「取引」そのものの観点から言っても、また、

発行者や採掘者や農家や生産者やエネルギーの発生者等が行う「情報開示」の観点から言っても、

「総合取引所」の下に複数の市場が存在することは投資家の利益を害さない、と私は思います。

私は、「総合取引所」という概念に完全に賛成ですし、「統合プロセスに干渉しないように。」と言いたいと思います。

{kind=link}

{kind=link}

{kind=link}

{kind=link}