2015年9月21日(月)

2015年9月21日(月)日本経済新聞

課税逃れ新ルール OECD決定へ きょうから租税委

(記事)

2015年9月21日(月)日本経済新聞

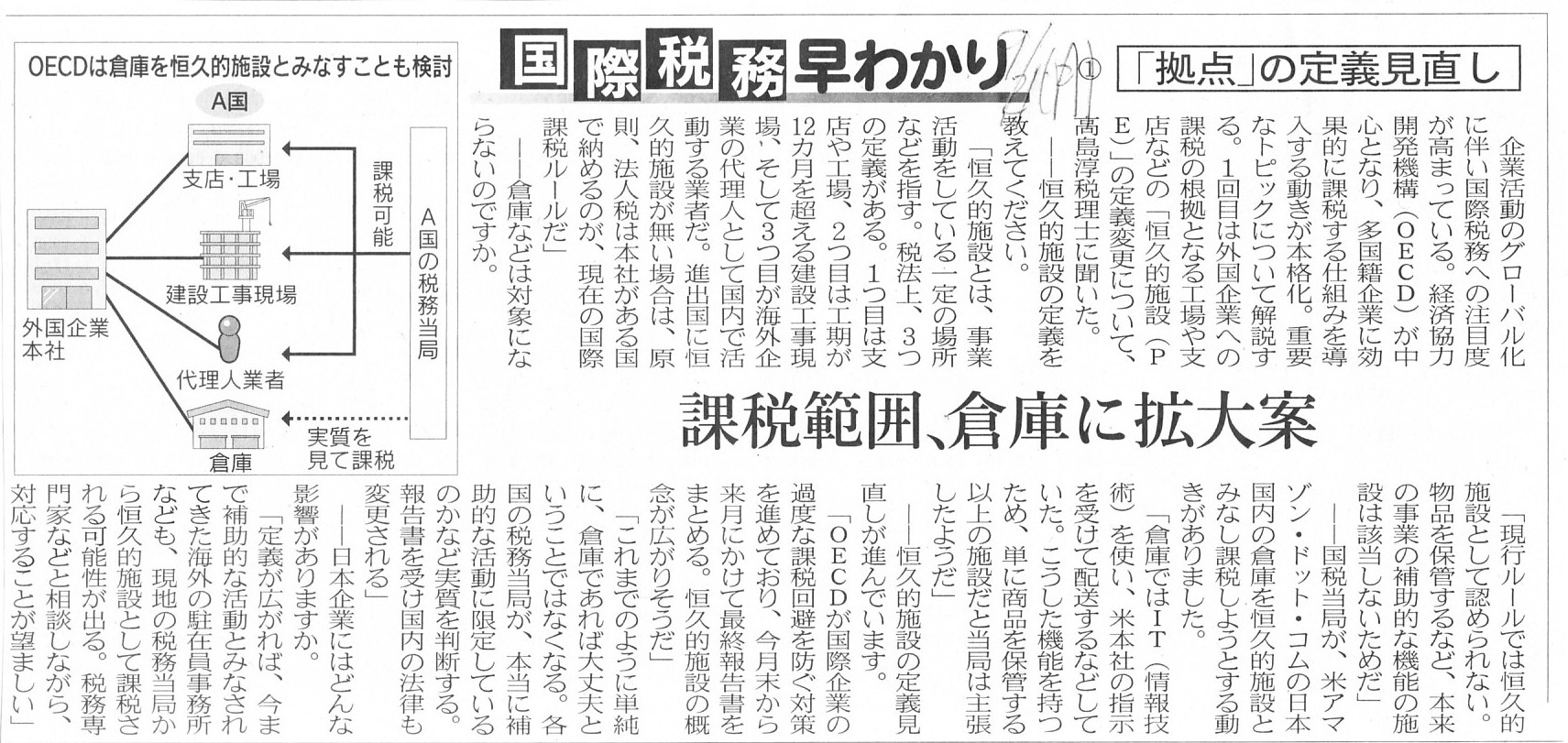

国際税務早わかり ①「拠点」の定義見直し

課税範囲、倉庫に拡大案

(記事)

過去の関連コメント

2015年9月1日(火)

http://citizen.nobody.jp/html/201509/20150901.html

【コメント】

The reason why assets which a company holds overseas are not

recorded in a balance sheet is

that the amount of the cost of the asset sold

or the acquisition cost of the asset which is transferred

is not recodrded in

a profit and loss statement.

The revenue is realized at the place where the

cost is accrued

and at the same time, the cost is accrued at the place where

the revenue is realized.

A company transfers domestically its asset which it

holds domestically.

Therefore, the revenue is recorded in a profit and loss

statement,

and the acquisition price is posted from a balance sheet to a

profit and loss statement

and as a result the cost is recorded in a profit

and loss statement.

A company is not able to transfer domestically its asset

which it holds overseas.

If so, the acquisition price is not posted from a

balance sheet to a profit and loss statement.

the cost is not recorded in a

profit and loss statement.

To put it simply, an asset account is to be a

cost.

After all, the revenue from an overseas asset is not recorded in a

profit and loss statement either, though.

After a fashion, a company can

record an asset which it holds overseas in a balance sheet.

Only to record in

a balance sheet can be done.

An overseas remittance is the acquisituion price

of the asset, that's all.

But, the problem occurs when a company intends to

transfer the asset.

For the revenue is realized overseas and the cost is

accrued overseas.

The link between a balance sheet and a profit and loss

statement is lost at the time of a transfer of the asset.

Therefore, a

company can't record an asset which it holds overseas in a balance

sheet,

because all of the assets which a company holds presuppose to be used

for a commercial transaction.

会社が海外に保有している資産が貸借対照表には計上されない理由は、販売された資産の原価の金額が、すなわち、

譲渡された資産の取得原価が、損益計算書に計上されなくなるからなのです。

収益は費用が発生する場所で実現しますし、また同時に、費用は収益が実現する場所で発生します。

会社は、国内に保有している資産を、国内で譲渡します。

ですから、収益が損益計算書に計上されるわけですし、また、取得価額が貸借対照表から損益計算書に転記されるわけです。

そしてその結果として、費用が損益計算書に計上されるわけです。

会社は、海外に保有している資産を国内で譲渡することはできません。

仮にそのようなことを想定しても、取得価額は貸借対照表から損益計算書に転記されないことになりますし、

費用が損益計算書に計上されないことになるのです。

簡単に言えば、資産勘定が費用になるのです。

結局のところは、海外資産からの収益もまた損益計算書には計上されないわけなのですが。

一応、会社は海外に保有している資産を貸借対照表に計上できます。

貸借対照表に計上するというだけならできはするのです。

海外送金額が資産の取得価額になるというだけなのです。

しかし、会社が資産を譲渡しようとする時に問題が発生するのです。

というのは、収益は海外で実現しますし、費用も海外で発生するからです。

貸借対照表と損益計算書のつながりが、資産の譲渡に際して、失われてしまうのです。

したがって、会社は、海外に保有している資産を貸借対照表に計上できないのです。

会社が保有している資産は全て、商取引で使用されるということを前提にしているのですから。

There doesn't exist the international taxation. There exists the domestic taxation only.

国際課税などありません。課税には一国内における課税しかありません。

"Holding proprty only" doesn't generate any revenues nor

expenses.

Revenues and expenses are not generated until a transfer of the

property.

「資産を保有しているだけ」では何の収益も費用も生じません。

資産を譲渡して初めて収益や費用が発生するのです。

The place where the revenue is realized, the place where the expense is

accured,

and the place where the Corporation Tax is levied are quite the same

place.

On the other hand, "only to hold property" is not a revenue, an

expense nor a tax base.

Therefore, without a transfer of property at all, a

company could be said

to be able to record an asset which it holds overseas

in a balance sheet.

収益が実現する場所、費用が発生する場所、そして法人税が徴税される場所というのは全て、完全に同じ場所なのです。

一方、「資産を保有するというだけ」では、収益でもありませんし費用でもありませんし課税標準でもありません。

したがって、仮に資産の譲渡を一切行わないならば、会社は海外に保有している資産を貸借対照表に計上できると言えるのです。

現代会計では、いわゆる固定資産の減価償却手続きや固定資産税といったものがあると聞いています。

それらやや変則的な手続きや租税のことを考慮しますと、

上記の議論は現代の課税に必ずしもそのまま当てはまるというわけではないと思います。

そう言えば、非常に非常に重要なことを今思い出しました。

いわゆる海外子会社の株式というのは、会社が海外に保有している資産の1つなのです。

なぜなら、海外子会社の株式というのは、海外の法律に基づいて発行されたものだからです。

海外子会社の株式は、海外資産なのです。

個別貸借対照表ベースで言えば、海外子会社の株式というのは言わば「保有しているだけ」だ、と言っても過言ではないのです。

その意味では、子会社株式売却益は、実際には個別損益計算書には計上されないのです。

というのは、海外子会社株式の実際の所有者は、親会社自身ではなく、現地の国の法律事務所といった海外の誰かなのですから。

新聞や雑誌では、「X社が海外子会社株式を取得した。」と書かれてあったり、

「Y社は当期に海外子会社株式売却益を計上する予定だ。」と書かれてあったりしますが、

会社は実際には、海外子会社株式を取得できませんし売却することもできないのです。

人―自然人と法人の両方を含む―は、現地の法律事務所といった現地の人を所有権のためのエミュレーター(擬似的な所有者)として

活用することによって、海外資産を擬似的に保有することしかできないのです。

海外送金によって、人は海外資産を擬似的に保有することができるようになったのです。

{kind=link}

{kind=link}