2018年8月30日(木)

2018年6月14日

株式会社キーエンス

有価証券報告書 第49期(平成29年3月21日-平成30年3月20日)

ttps://www.keyence.co.jp/download/directDownload/?asrc=gyBAvbFX%2FZH7g0c32HgFjjMDRd8SMBrD

(ウェブサイト上と同じPDFファイル)

2018年6月22日

株式会社ミツバ

有価証券報告書 第73期(平成29年4月1日-平成30年3月31日)

ttps://www.mitsuba.co.jp/cms/jp/wp-content/uploads/ir/pdf/180625_edinet.pdf

(ウェブサイト上と同じPDFファイル)

Relationship between cash flows from operating activities and investments

in plant and equipment.

営業活動によるキャッシュフローと設備投資との関係

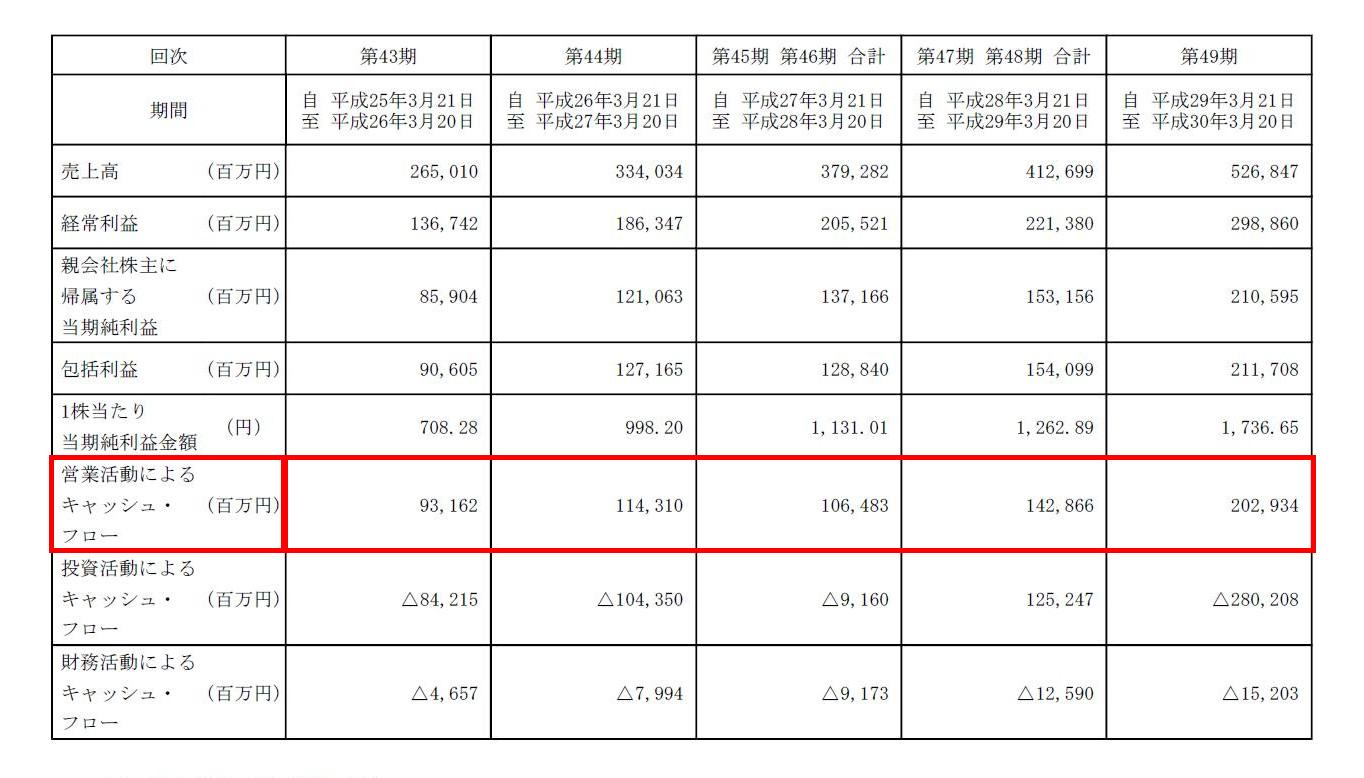

株式会社キーエンス

第一部【企業情報】

第1 【企業の概況】

1【主要な経営指標等の推移】

(1) 連結経営指標等

(6/68ページ)

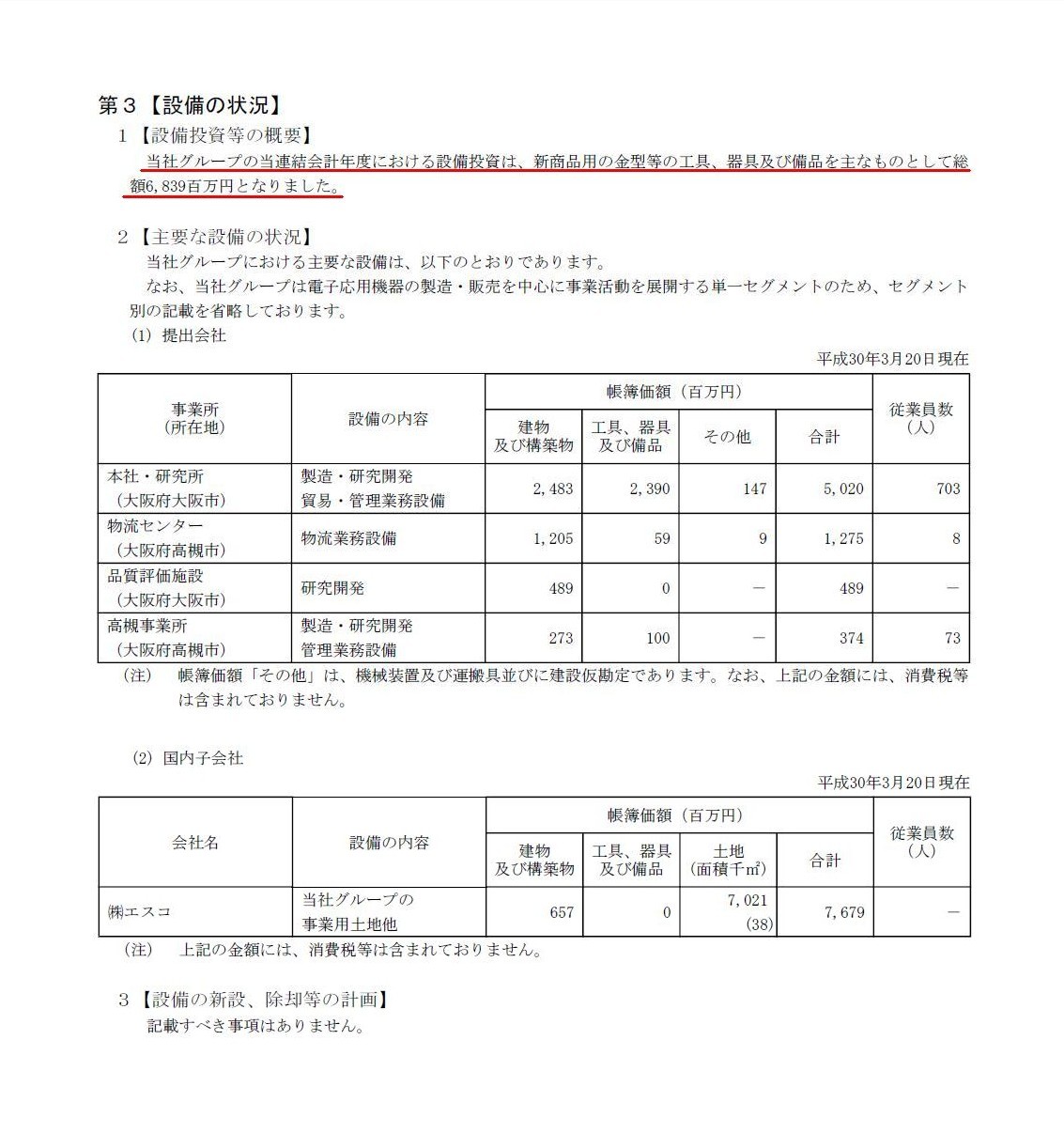

第3 【設備の状況】

(16/68ページ)

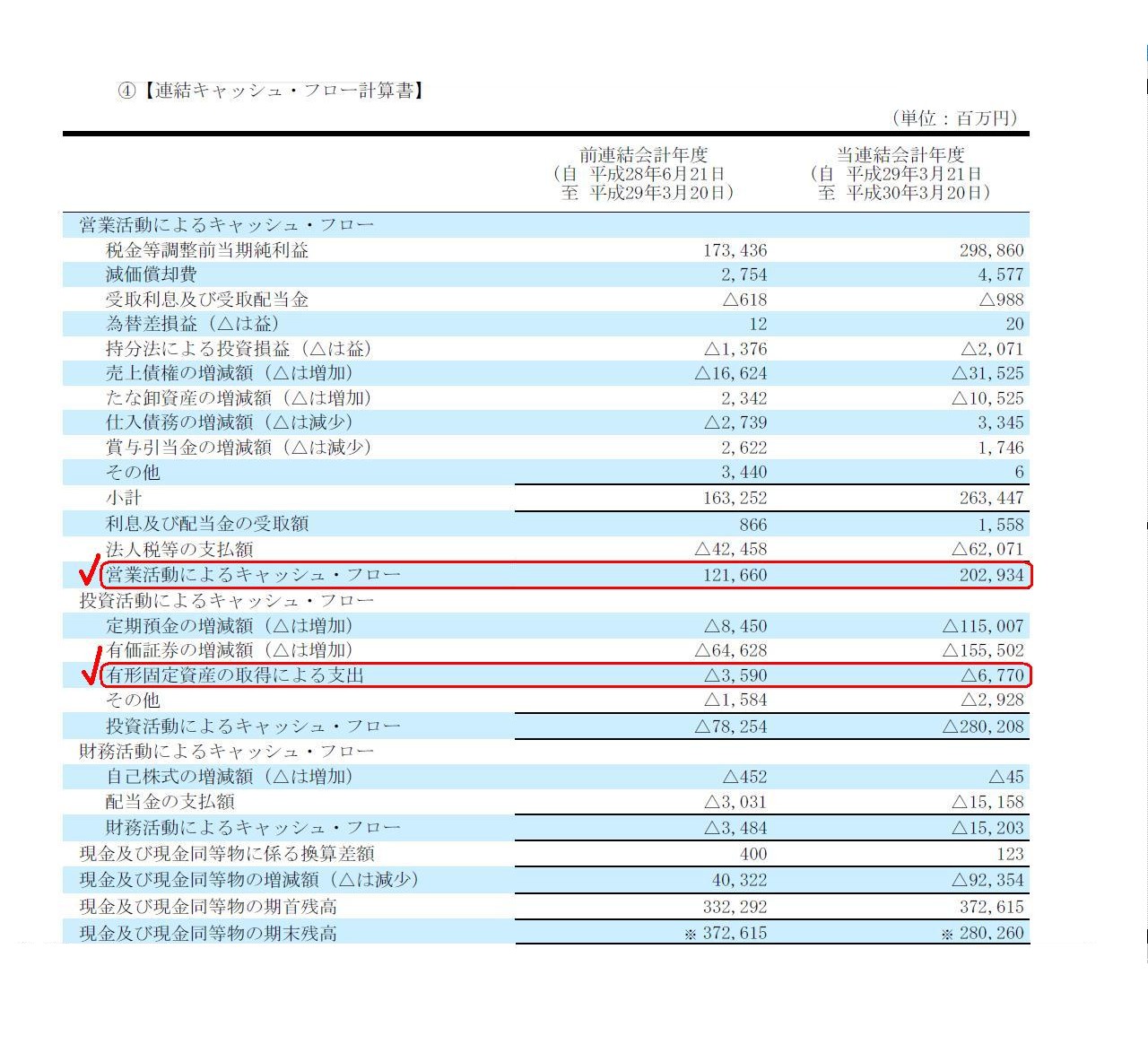

第5 【経理の状況】

1【連結財務諸表等】

(1) 【連結財務諸表】

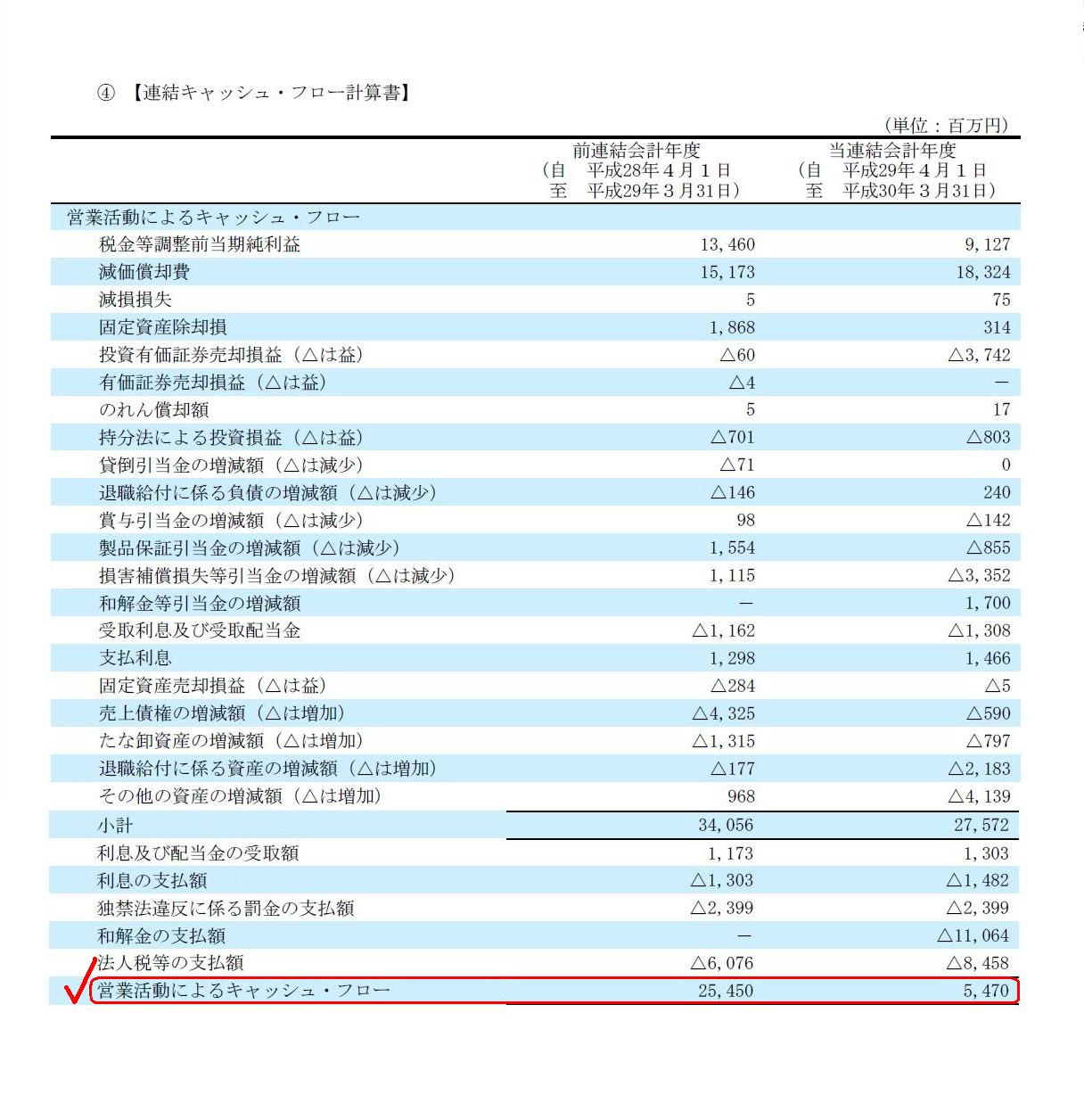

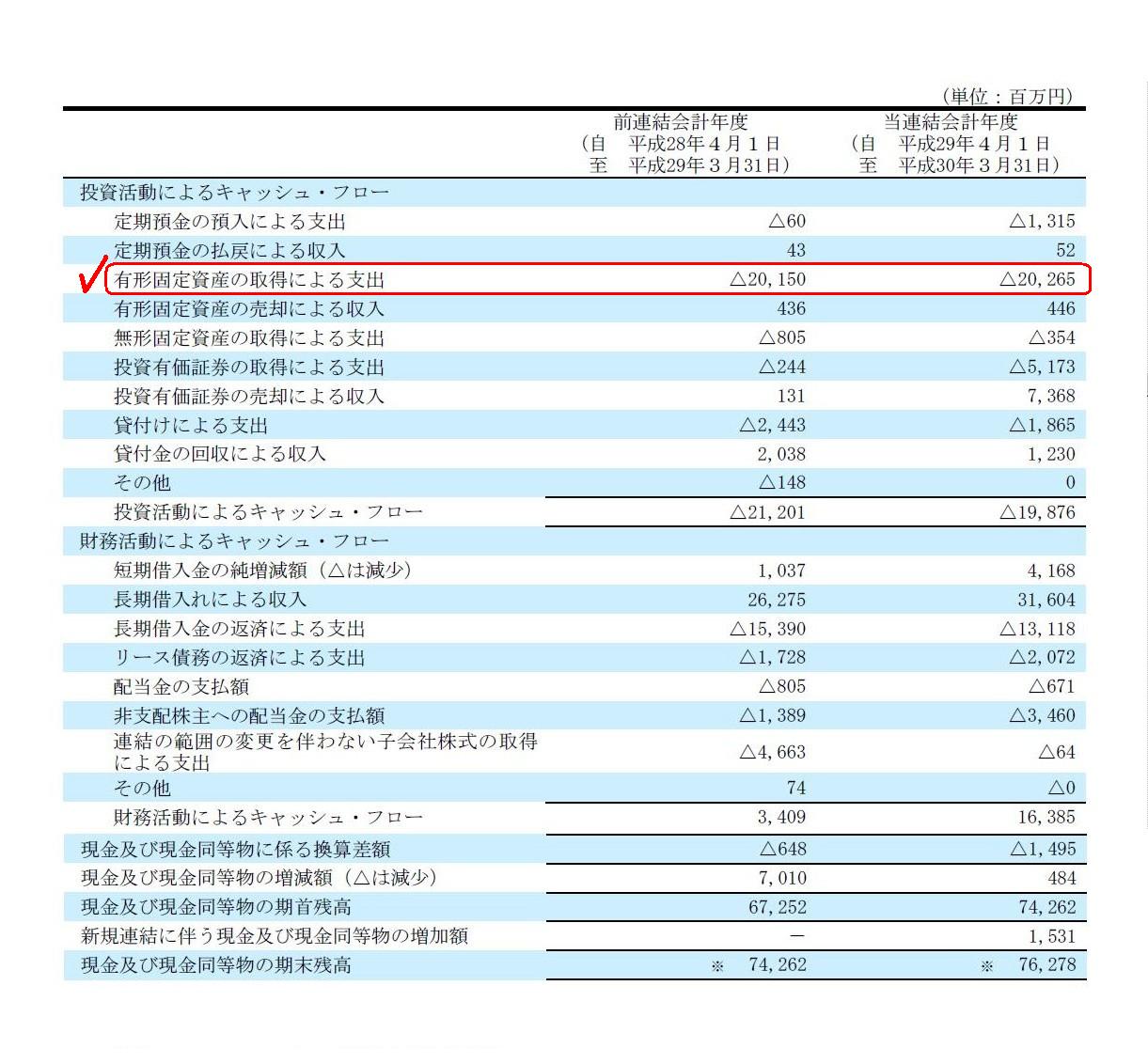

④【連結キャッシュ・フロー計算書】

(36/68ページ)

株式会社ミツバ

第一部【企業情報】

第1 【企業の概況】

1【主要な経営指標等の推移】

(1) 連結経営指標等

(2/104ページ)

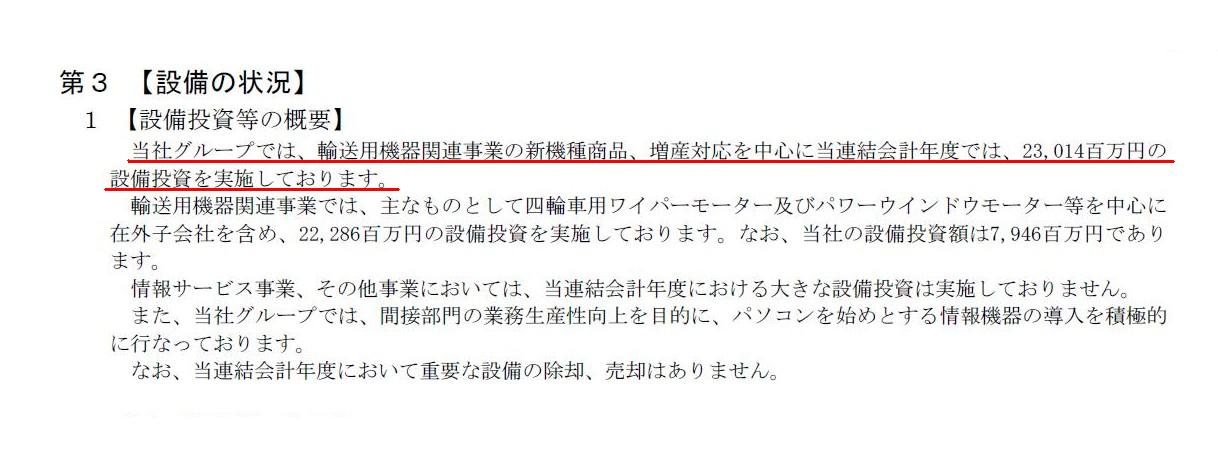

第3 【設備の状況】

1 【設備投資等の概要】

(20/104ページ)

第5 【経理の状況】

1【連結財務諸表等】

(1) 【連結財務諸表】

④【連結キャッシュ・フロー計算書】

(47/104ページ)

(48/104ページ)

Cash flows from operating activities are routine.

That is to say, when a

company operates normally,

the amount of cash flows from operating

activities of each business year is approximately equal to each other.

On the

other hand, investments in plant and equipment are never routine.

That is to

say, even when a company operates normally,

the amount of investments in

plant and equipment of each business year is quite irregular.

For a useful

life of buildings, structures, machinery and equipment, vehicles, fixtures,

fittings,

tools and equipment is completely different from each other.

A

company operates every business year,

whereas a company doesn't invest in

plant and equipment every business year.

A company invests in plant and

equipment every several years or every several ten years.

the amount of cash

flows from operating activities of one business year

and that of investments

in plant and equipment of the business year are never in one-to-one

correspondence.

Therefore you can't divide the amount of investments in plant

and equipment of one business year

by that of cash flows from operating

activities of one business year.

The ratio of the former to the latter is

completely nonsense.

There is no consistency between a numerator and a

denominator in the ratio.

To begin with, it is a matter of course that the

ratio above is inconsistent.

For plant and equipment are depreciable

assets.

Operating revenues and costs in general are recorded in each business

year (i.e. they are fully recorded in one year),

whereas the costs of plant

and equipment are recorded regularly over a useful life of the respective

assets.

That's why the ratio above is nonsense.

営業活動によるキャッシュフローは経常的なものです。

すなわち、会社が事業を正常に営んでいる時は、

各事業年度の営業活動によるキャッシュフローの金額は毎年概ね同じになります。

一方、設備投資は決して経常的なものではありません。

すなわち、たとえ会社が事業を正常に営んでいようとも、各事業年度の設備投資の金額は全く不規則なものとなります。

というのは、建物、構築物、機械装置、車両運搬具、工具、器具及び備品の耐用年数は、それぞれ完全に異なっているからです。

会社は毎年事業を営みますが、会社は毎年設備投資を行うわけではありません。

会社は、数年毎もしくは数十年毎に設備投資を行うのです。

ある事業年度の営業活動によるキャッシュフローの金額とその事業年度の設備投資の金額は、

決して一対一に対応してはいないのです。

したがって、ある事業年度の設備投資の金額をその事業年度の営業活動によるキャッシュフローの金額で

割り算をすることはできないのです。

設備投資と営業活動によるキャッシュフローの比率というのは全く意味がないのです。

その比率には、分子と分母との間に整合性が全くないのです。

そもそもの話、上記の比率に整合性がないのは当たり前のことなのです。

というのは、設備というのは減価償却資産だからです。

営業上の収益と費用全般は事業年度毎に計上されます(すなわち、それらは全額が1事業年度に計上されます)が、

設備の費用は、各資産の耐用年数に渡って規則的に計上されるのです。

そういうわけで、上記の比率には意味がないのです。

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}