原産地規則ポータル - 税関

ttp://www.customs.go.jp/roo/

原産地規則の概要(財務省関税局・税関 2017年9月)

ttp://www.customs.go.jp/roo/origin/gaiyou.pdf

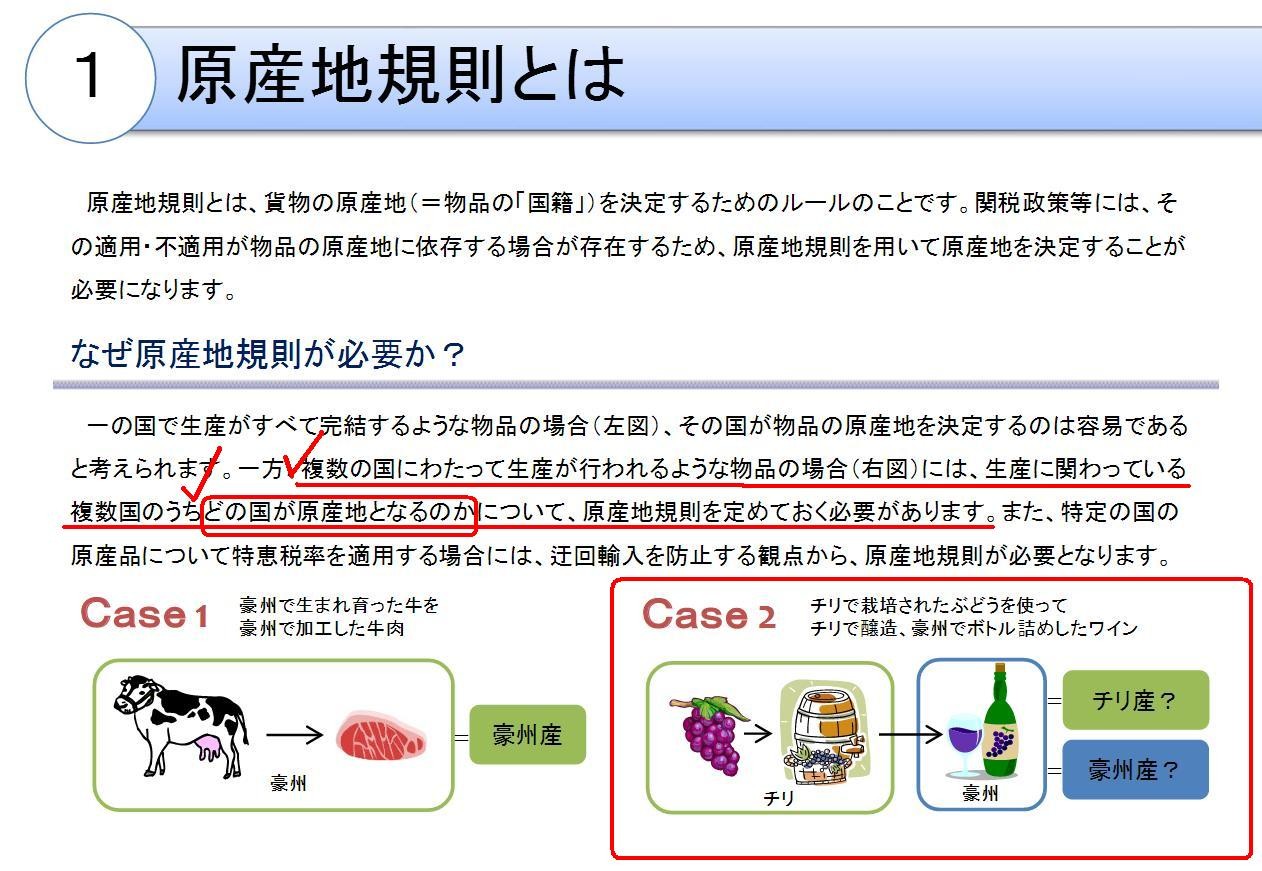

原産地規則とは

(3/11ページ)

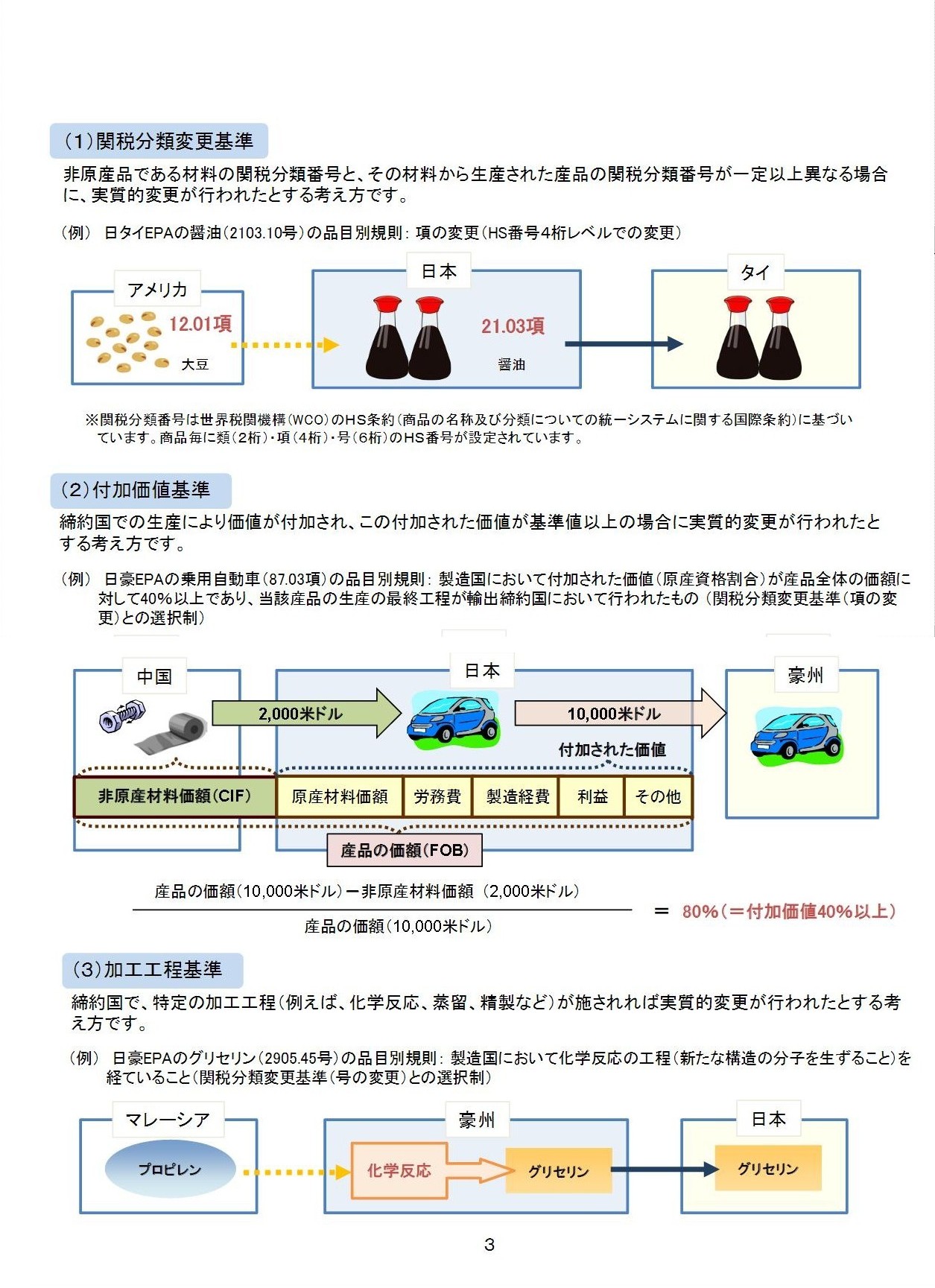

実質的変更基準を満たす産品

(1)関税分類変更基準

(2)付加価値基準

(3)加工工程基準

(5/11ページ)

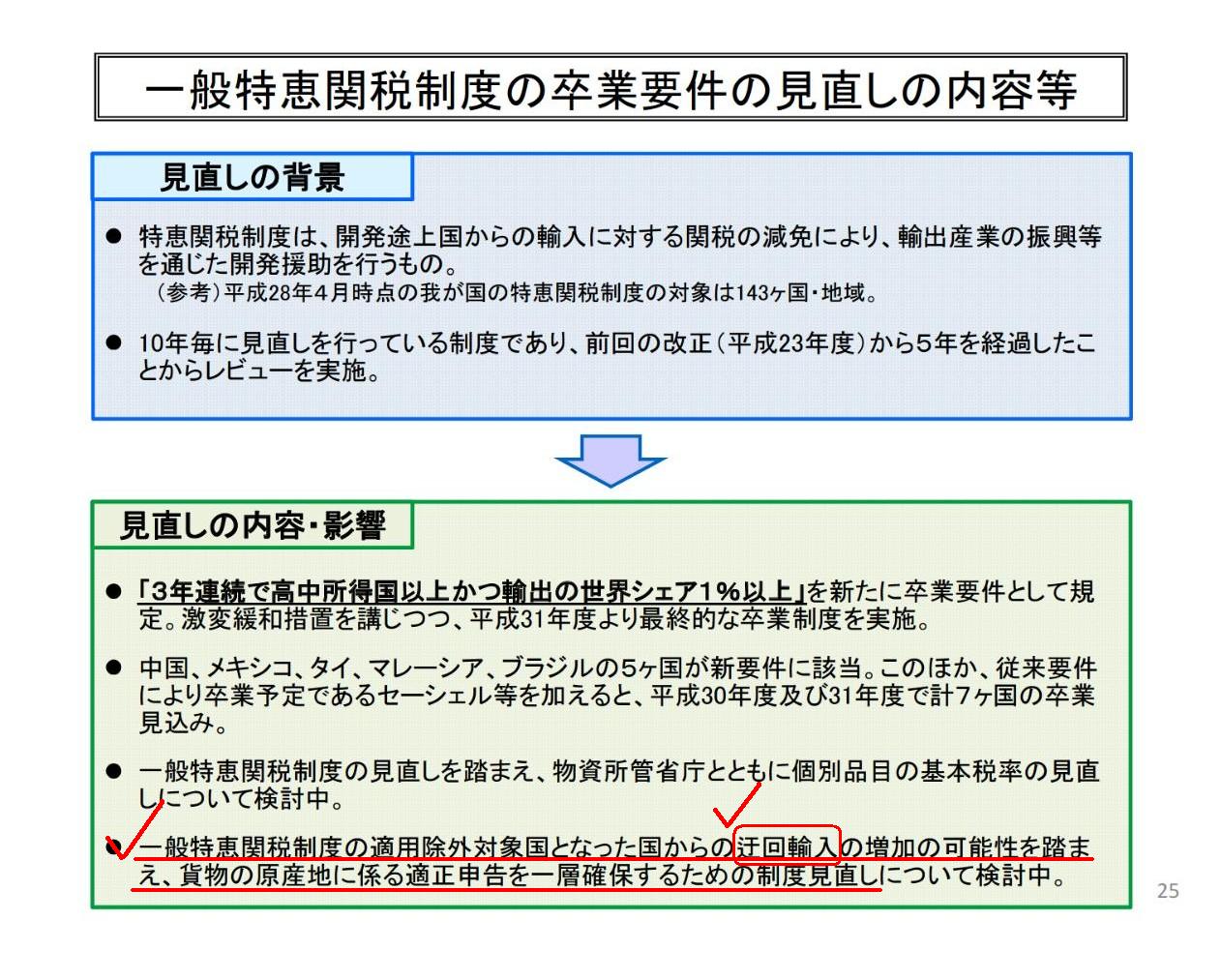

> 一般特恵関税制度の見直しを踏まえまして、物資所管省庁とともに個別品目の基本税率の見直しについて

>現在検討しているところでございます。一般特恵関税制度の見直しを行いますと、

>特恵関税が適用されなくなって税率が上がるわけですが、他方において、我が国利用者の利便の観点から、

>低い税率のまま留め置くことがむしろ妥当だと判断される品目については、基本税率そのものを引き下げる

>ということで対応することもあり得まして、どのようなものについてそのような対応をすることが妥当かということを

>検討しているところでございます。

> 一番下のポツは、一般特恵関税制度の適用除外対象国となった国から、今度、迂回輸入が増加するおそれがあり、

>この特恵関税制度を適用するためには、原産地をきちんと確認することが一層重要になるということでございまして、

>そのための制度見直しを現在検討しているところでございます。

(資料1)最近の関税政策・税関行政を巡る状況

ttp://www.mof.go.jp/about_mof/councils/customs_foreign_exchange/

sub-of_customs/proceedings_customs/material/20171003/kana20171003siryo1.pdf

一般特恵関税制度の卒業要件の見直しの内容等

(26/57ページ)

On the principle of law, the authorities know

not only interested parties

of a transaction but also details of an object of the transaction.

法理的には、当局は、取引の当事者について知っているだけではなく、取引の目的物の詳細についても知っているのです。

From a standpoint of a Japanese importer, whether imported goods which it

purchased from abroad

has come to Japan by a roundabout route or not has

nothing to do with its own import business.

日本の輸入業者の立場から言えば、自社が海外から購入した輸入品が迂回して日本にやってきたかどうかは、

自社の輸入業とは全く関係がないことなのです。

In theory, a tariff rate is determined uniquely

only by a passing

route "from the customs in Country X to the customs in Country Y."

理論的には、関税率は、「X国の税関からY国の税関へ」という通行した航路のみで一意に決まるのです。

All a human being can see is a name of the customs.

人間には関税の名前しか分からないのです。

In theory, a tariff has no concept "place of origin" in it

because a

manufacturer produces goods in a "country where the production cost is the

lowest" from the beginning.

And, from a standpoint of an exporter,

it

exports goods from a "country where the total cost of the exported goods is the

lowest" from the beginning.

After all, the difference of a tariff rate

enables an exporter to be inclined to take a roundabout route.

To be honest

with this problem, it is the custom authorities themselves that cause the

"commodity shunting" at issue.

理論的には、関税には「原産地」という概念はないのです。

なぜならば、製造業者は、始めから「生産コストが最も小さくなる国」で物を生産するからです。

そして、輸出する者の立場から言えば、物品の輸出は始めから「輸出品の総コストが最も小さくなる国」から行うものなのです。

結局のところ、関税率に差異があるので、容易に輸出業者は迂回航路を通りたくなってしまっているのです。

この問題点について率直に言えば、論点となっている「迂回貿易」を引き起こしているのは、税関当局そのものなのです。

{kind=link}

{kind=link}

{kind=link}