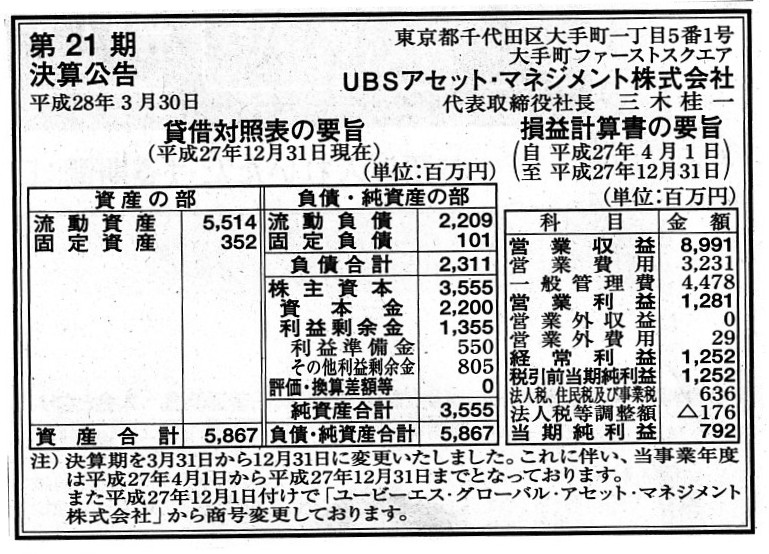

2016年3月30日(水)

2016年3月30日(水)日本経済新聞 公告

第21期決算公告

UBSアセット・マネジメント株式会社

(記事)

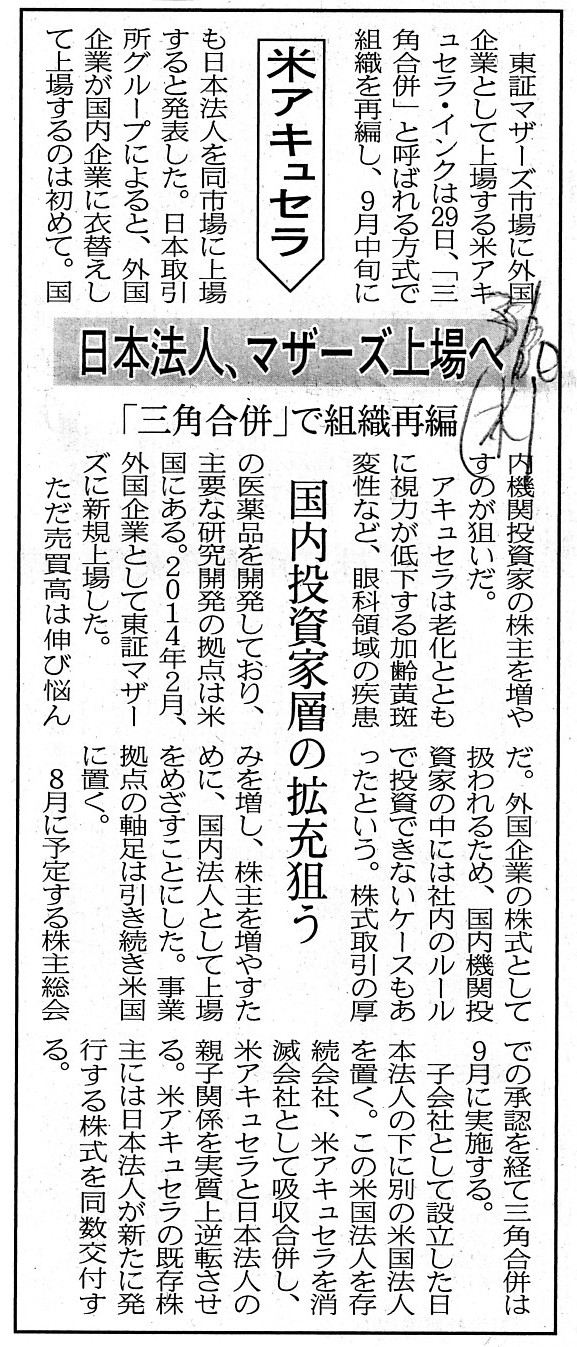

2016年3月30日(水)日本経済新聞

米アキュセラ 日本法人、マザーズ上場へ 「三角合併」で組織再編 国内投資家層の拡充狙う

(記事)

2016年3月29日

アキュセラ・インク(Acucela

Inc.)

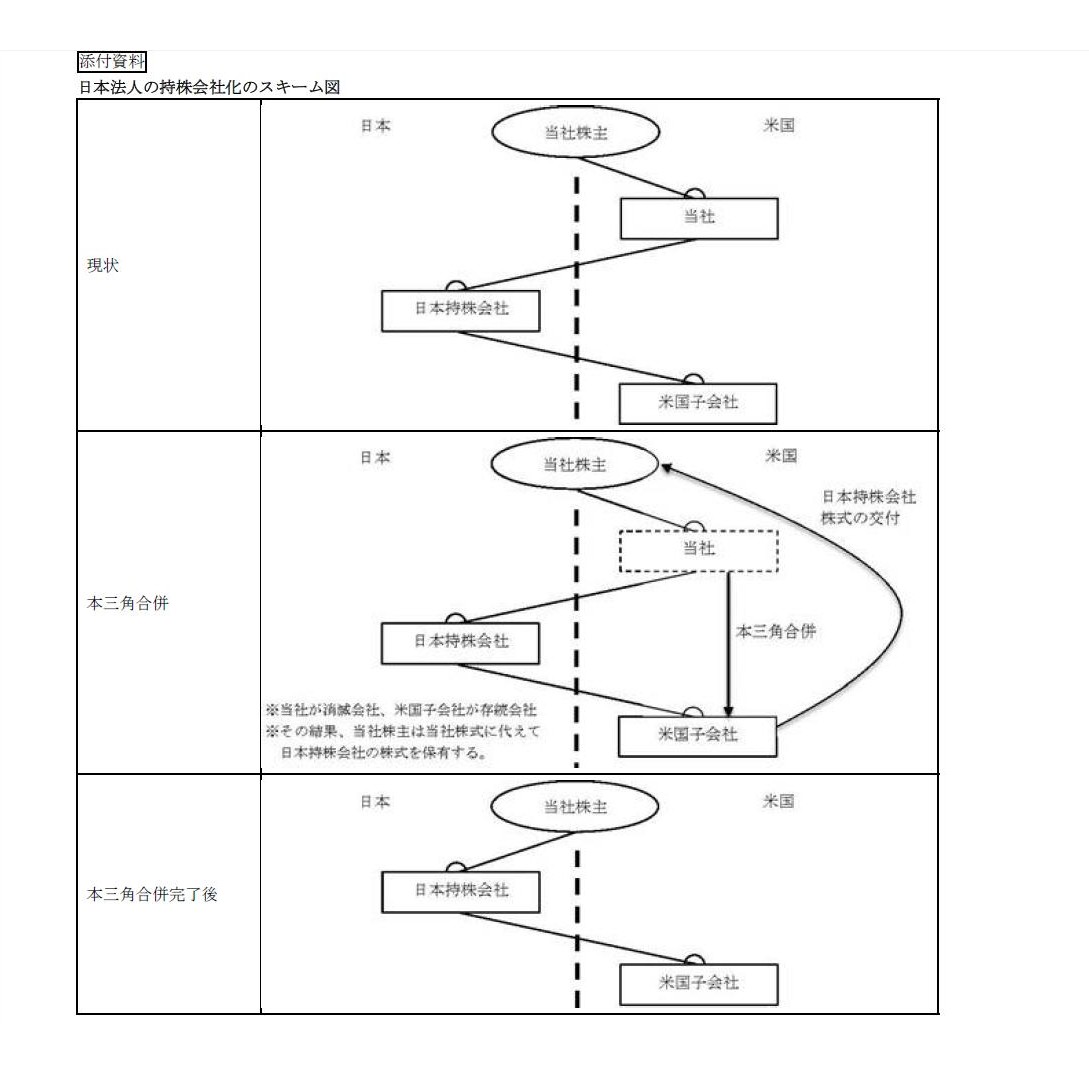

三角合併による日本法人の持株会社化、内国株式としての上場申請および付属定款の一部変更のお知らせ

ttp://contents.xj-storage.jp/xcontents/AS80242/94afbe49/937b/4a81/ba1b/10246bdc9680/140120160328444262.pdf

(サイト上とPDFファイル)

2016年3月30日

アキュセラ・インク(Acucela

Inc.)

臨時報告書

ttp://contents.xj-storage.jp/xcontents/AS80242/48f33872/bcf2/4f9e/883d/abcb585f586c/S10079RZ.pdf

(サイト上とPDFファイル)

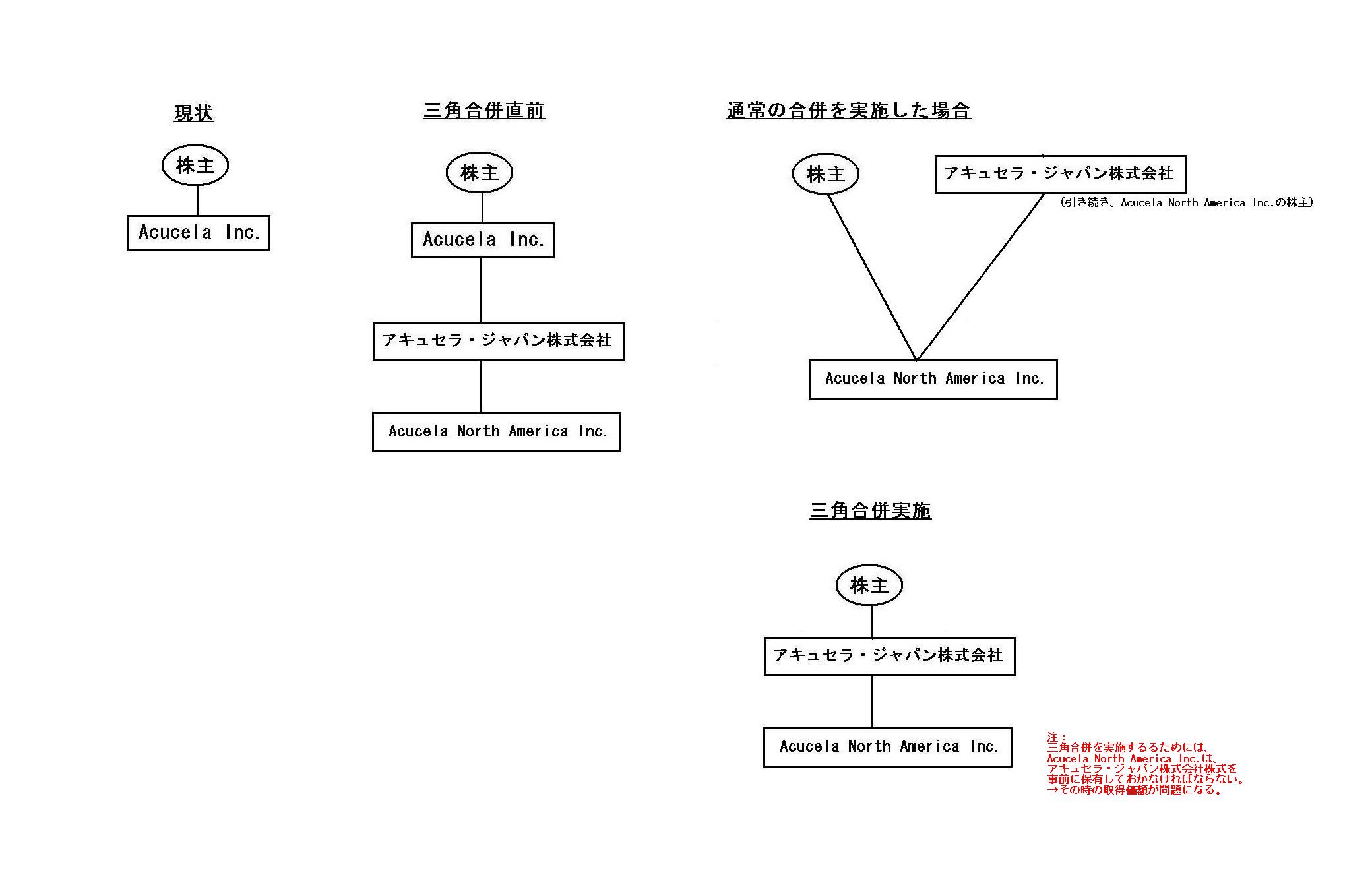

日本法人の持株会社化のスキーム図

(7/7ページ)

【コメント】

取引の流れが非常に分かりづらいかと思いますので、図に描いてみました。

「現状、三角合併直前、通常の合併を実施した場合、三角合併実施」

注:

三角合併を実施するるためには、Acucela

North America

Inc.は、

アキュセラ・ジャパン株式会社株式を事前に保有しておかなければならない。

→その時の取得価額が問題になる。

論点は論じだすときりがないくらい多数あろうかと思います、

私が1つ気になったのは、三角合併の際に存続会社が消滅会社株主に割当交付する”他社株式”のことです。

ここで言う”他社株式”とは、「アキュセラ・ジャパン株式会社株式」のことになるわけですが、

存続会社は「アキュセラ・ジャパン株式会社株式」をいくらで取得するのだろうか、と思いました。

また、存続会社は消滅会社株主に「アキュセラ・ジャパン株式会社株式」を合併の対価として割当交付するわけですが、

その時の「対価の価額」はいくらになるのだろうか、と思いました。

存続会社にとって、「対価の価額」は「取得価額」と同じ、でよいのでしょうか。

この点について考えを深めていくと、「等価交換」の意味が分かったような気がします。

結論を先に言えば、「等価交換」とは目的物と現金の交換です。

目的物と目的物の交換、すなわち、物々交換は、概念的・心理的には等価交換かもしれませんが、

少なくとも会計上は等価交換ではないのです。

どの会社の株式が上場しているのですか?

Acucela North America Inc. somehow acquires Acucela Japan KK's shares

beforehand

and transfers the shares to shaerholders of Acucela Inc.

Acucela North America Inc.は何らかの手段により事前にアキュセラ・ジャパン株式会社株式を取得し、

そしてAcucela

Inc.株主に対しその株式を譲渡します。

But, Acucela North America Inc. does so as consideration of the merger.

In

other words, Acucela North America Inc. does not record any profits nor losses

on a sale of the shares.

All Acucela North America Inc. records as a profit

or a loss on the merger is a difference between

the debit side (assets

succeeded) and the credit side (liabilities succeeded and Acucela Japan KK's

shares delivered).

At this point, the value of Acucela Japan KK's shares is

considered unchangeable

from the acquisiion to the delivery.

How can you

say that a value of the shares at the point of the delivery is

equal to a

value of the shares at the point of the acquisition?

For example, let's think

that parties make barter.

At first, one party acquires an asset at 100

yen.

The value of the asset is 100 yen.

Then, one party and the other

party make barter.

One party receives a certain asset from the other party

and gives his asset to the other party.

Concerning this transaction, on the

accounting, one party transfers his asset without a consideration

and

acquires a certain asset without a consideration.

For a value of a certain

asset which one party acquires from the other party is unknown.

To put it

simply, this transaction is not an equivalent exchange, actually.

Barter is

not an equivalent exchange.

It is true that both of the parties mutually

acknowledge this transaction to be a fair exchange

and to be an exchange of

equal value.

Conceptually speaking, this transaction may be an equivalent

exchange.

But, on the accounting, this transaction not an equivalent

exchange.

Frankly speaking, all you can exchange your object for is

cash.

An exchange of an object for cash, that is called an equivalnet

exchange.

An exchange of an object for another object is not called an

equivalnet exchange.

An exchange of an object for another object is literally

barter, that's all.

An object itself does not have a value.

But, an object

which is exchanged for cash has a value.

The term "equivalent" means "have the equal value."

How much is

love?

Nobody can answer.

The reason why nobody can answer the question is

not that love is pricelss (i.e. extremely precious),

but that nobody pays nor

receives cash in exchange for love.

To conclusion, an equivalent exchange

only, or an exchange of an object for cash only,

is a subject of the

accounting.

It means that a person doesn't make a journal entry such as

(an object received) 100 yen / (an object transferred) 100 yen

on barter.

A person makes a journal entry such as

(an object received) 0

yen

/ (cash) 0 yen

(loss on a sale of an object) 100 yen

(an object transferred) 100 yen

on barter.

An object transferred has a value because he pays cash in

exchange for the object.

But, an object received doesn't have a value because

he does not exchange his object for cash.

The former transaction is exactly

an equivalent exchange,

but the latter transaction is not an equivalent

exchange.

しかし、Acucela North America Inc. がそうしたのは、合併の対価としてであるわけです。

他の言い方をすれば、Acucela

North America Inc. は、株式の売却益も売却損も計上しないわけです。

Acucela North America Inc.

が合併に際して利益や損失として計上するのは、

借方(承継した資産)と貸方(承継した負債と交付したアキュセラ・ジャパン株式会社株式)の差額のみなのです。

この時、アキュセラ・ジャパン株式会社株式の価額は、取得から交付までの間、変化はしないと考えられているわけです。

交付時点における株式の価額は、取得時点における株式の価額と同じであると、なぜ言えるのでしょうか。

例えば、当事者が物々交換を行うことについて考えてみましょう。

まず最初に、一方の当事者が資産を100円で取得するとします。

この資産の価額は100円です。

その上で、一方の当事者と相手方とが物々交換をするとします。

一方の当事者は、相手方からある資産を受け取り、そして自分の資産を相手方に渡します。

この取引に関して言えば、会計上は、一方の当事者は自分の資産を無償で譲渡したことになりますし、

そして、ある資産を無償で取得したことになるわけです。

なぜなら、一方の当事者が相手方から取得したある資産の価額というのは不明であるからです。

簡単に言えば、実はこの取引は等価交換ではないのです。

物々交換は等価交換ではないのです。

確かに、当事者は両者とも、相互に、この取引は公平な交換であると認めていますし、等しい価値を持った交換であると認めています。

概念的に言えば、この取引は等価交換なのかもしれません。

しかし、会計上は、この取引は等価交換ではないのです。

率直に言えば、目的物と交換することができるものというのは、現金だけなのです。

目的物と現金の交換、それを等価交換と呼ぶのです。

目的物と目的物の交換は、等価交換とは呼ばないのです。

目的物と目的物の交換は、文字通り、物々交換だ、というだけのです。

目的物それ自体には、価額はないのです。

しかし、現金と交換された目的物には価額があるのです。

「equivalent」という言葉は、「同じ価値がある」という意味です。

愛はいくらでしょうか。

誰も答えられません。

その質問に誰も答えられない理由は、愛は値踏みができないもの(すなわち、極めて貴重なもの)だからではなく、

愛と交換に現金を支払ったり受け取ったりはしていないからなのです。

結論を言えば、等価交換のみが、すなわち、目的物と現金の交換のみが、会計の対象なのです。

つまり、物々交換を行った時、

(受け取った目的物) 100円 / (引き渡した目的物) 100円

というような仕訳は切らないのです。

物々交換を行った時は、

(受け取った目的物) 0円 / (現金) 0円

(目的物の売却損) 100円 (引き渡した目的物) 100円

という仕訳を切るわけです。

引き渡した目的物には、価額はあります。

なぜなら、その目的物と交換に現金を支払ったからです。

しかし、受け取った目的物には価額はありません。

なぜなら、目的物と現金を交換していないからです。

前者の取引はまさに等価交換ですが、後者の取引は等価交換ではないのです。

{kind=link}

{kind=link}

{kind=link}

{kind=link}