2015年12月14日(月)

2015年10月31日(土)日本経済新聞

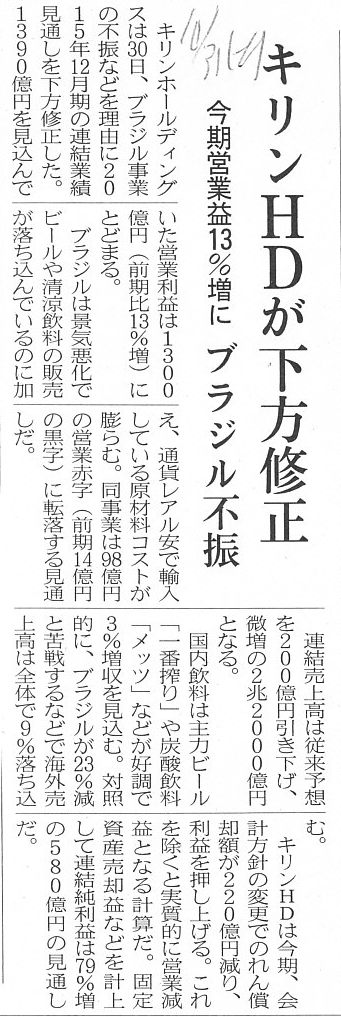

キリンHDが下方修正 今期営業益13%増に ブラジル不振

(記事)

2015年10月30日

キリンホールディングス株式会社

2015年12月期第3四半期決算短信〔日本基準〕(連結)

ttp://www.kirinholdings.co.jp/irinfo/library/tansin/pdf/2015_3q_tanshin.pdf

プレゼンテーション資料

ttp://www.kirinholdings.co.jp/irinfo/event/explain/pdf/2015_3q_presentation.pdf

「2015年12月期第3四半期決算短信〔日本基準〕(連結)」

2.

サマリー情報(注記事項)に関する事項

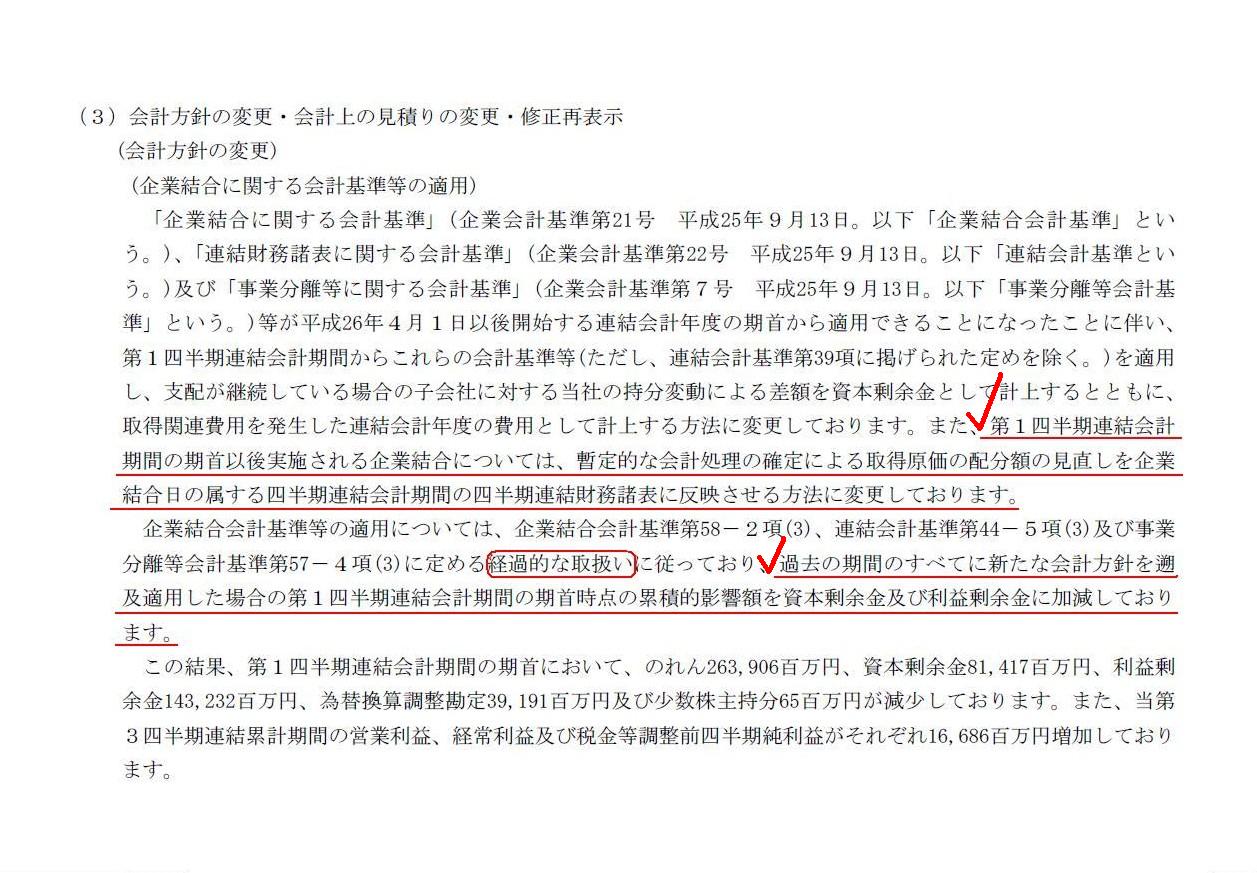

(3)会計方針の変更・会計上の見積りの変更・修正再表示

(会計方針の変更)

(企業結合に関する会計基準等の適用)

(8/28ページ)

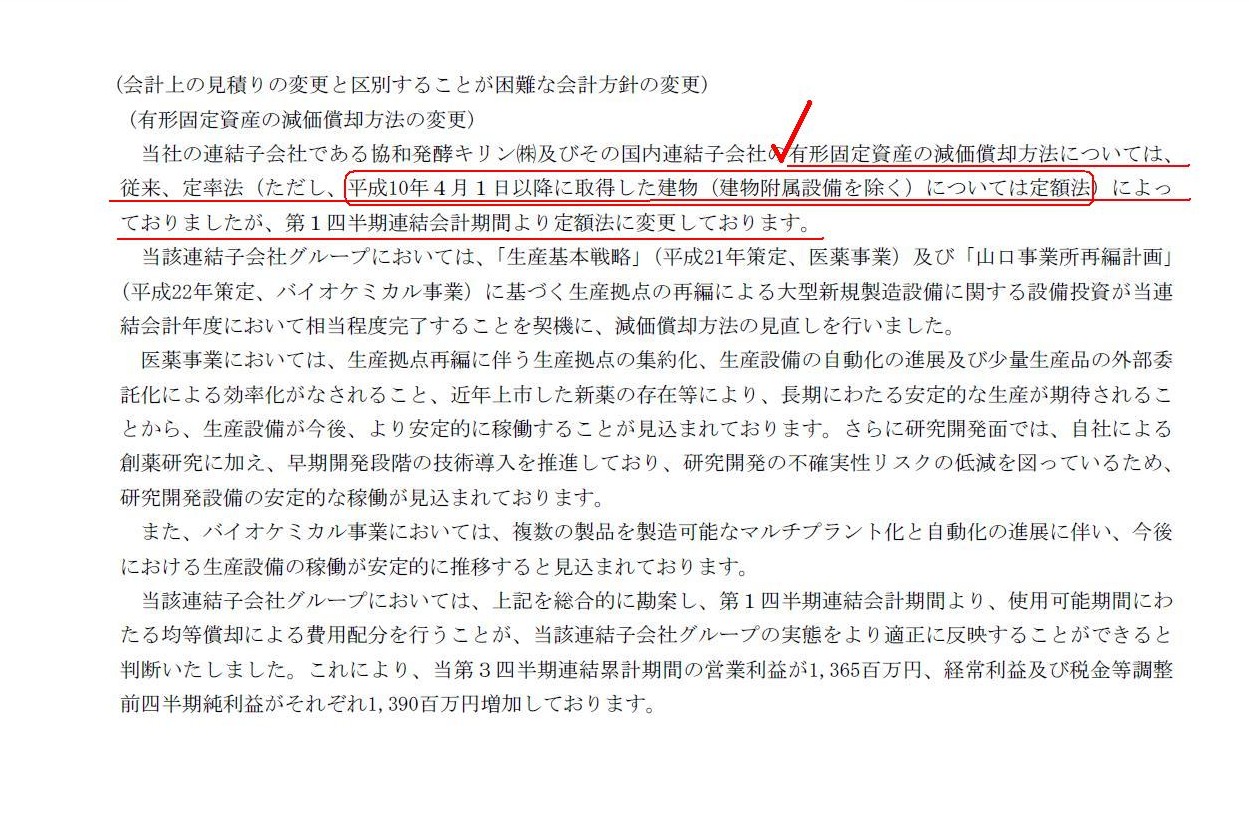

(会計上の見積りの変更と区別することが困難な会計方針の変更)

(有形固定資産の減価償却方法の変更)

(9/28ページ)

【コメント】

記事には、キリンホールディングス株式会社の2015年12月期の業績見通しに関連して、

>キリンHDは今期、会計方針の変更でのれん償却額が220億円減り、利益を押し上げる。

と書かれています。

決算短信には、この点については、8/28ページと9/28ページに詳細な記載があります。

また、財務諸表の注記にも、適用する会計基準の変更に伴い、

株主資本の金額に著しい変動が生じていること(14/28ページ)や

のれんの金額に重要な変動が生じていること(15/28ページ)について注記があります。

注記には、適用する会計基準の変更に伴い、各基準に定めてある「経過的な取扱いに従っております。」と書かれています。

他にも、いくつかの場所に、適用する会計基準の変更を受け、「経過的な取扱いに従っております。」という記載があります。

私がこれらの記載を読んで思ったのは、「経過的な取扱い」という部分や

「過去の期間のすべてに新たな会計方針を遡及適用した場合」という部分です。

法律の世界では、法の遡及適用は当然のこととして禁止されているわけですが、

会計の世界では、会計基準の遡及適用についてはどのように考えるべきなのだろうか、と思いました。

企業会計基準そのものに遡及適用に関する定めがあるくらいですから、

法律とは異なり、会計では遡及適用を行うものである、というふうに考えてしまいます。

もしくは、会計基準が改正されたならば、

会社の全てに(会社の資産負債、権利義務全てに)当然に新しい(改正後の)会計基準が適用されるもの、と考えてしまいます。

改正前の古い会計基準を会社に適用することが、何か遡及適用なのではないか、と感じてしまうかもしれません。

この点について、法理的な観点から考えてみましたところ、私としましては、

適用するべき会計基準は会社単位ではなく取引単位だ、という結論に達しました。

会計基準が改正されても、会社全体に(会社の資産負債、権利義務全てに)適用されるのではなく、

改正後の取引のみに改正後の会計基準が適用される、という考え方が正しいのではないか、と思いました。

逆から言えば、改正前の取引には、会計基準改正後も従来通り改正前の会計基準が適用される、となります。

私のこの考えを法律面から捉えれば、会計基準の適用は取引単位、

会計面から捉えれば、会計基準の適用は勘定単位、となります。

私のこの考えに基づくと、計算書類に新旧複数の会計基準が適用される、ということになります。

他の言い方をすれば、同一の計算書類に、改正前の会計基準に従った会計処理と改正後の会計基準に従った会計処理の両方が含まれる、

ということになります。

財務情報開示の観点からは、どちらの計算書類の方が望ましいかは一言では答えは出ない部分もありますが、

少なくとも法理的な観点から言えば、会計処理方法は取引毎に決まると考えるため、

改正前の会計基準に従った会計処理と改正後の会計基準に従った会計処理が計算書類内に混在するのはやむを得ない、

ということになろうかと思います。

会社ではなく取引で決まる、これが今日導き出した結論になります。

取引に対しある会計基準を適用した後は、その取引に伴い発生した・計上された勘定が消滅もしくは完了するまでは、

その会計基準を変更することは行ってはなりません。

As at which date did a company acquire the tangible fixed asset?

どの日付で会社は有形固定資産を取得したのですか。

In case a company acquired a tangible fixed asset as at April 1st,

1998,

the depreciation of the tangible fixed asset should be made

in

accordance with the Corporation Tax Act of April 1st, 1998,

even if the

Corporation Tax Act is amended afterwards.

会社が有形固定資産を平成10年4月1日付けで取得した場合は、たとえその後法人税法が改正されようとも、

その有形固定資産の減価償却手続きは平成10年4月1日時点の法人税法に従って行わなければなりません。

The description below is my opinion, though.

A transaction corresponds to

an accounting standard one-to-one.

One set of financial statements doesn't

correspond to an accounting standard one-to-one.

In short, one set of

financial statements is prepared in accordance with plural accounting

standards

which include both the old (repealed) accounting standards and the

new (amended) accounting standards.

The new (amended) accounting standard is

not applied to

the old transaction (i.e. already-recorded accounts on the

accounting).

Whether the new (amended) accounting standard is applied or

not

depends not on financial statements the concerned period but on a

transaction itself.

In other words, which accounting standard is applied is

determined not by financial statements but by a transaction itself.

For, when

the initial journal entry on a transaction (for example, the acqcuisition of a

tangible fixed asset) is made,

a series of the following journal entries on

the transaction (in this case, the depreciation of the tangible fixed

asset)

in accordance with the accounting standard as at the transaction is

scheduled to be made.

And, in case the quite new (not amended but

newly-provided) accounting standard

on the valuation of securities in a

market value method is enforced,

the new accounting standard is not applied

to securites which a company has owned since before the enforcement

and it is

applied only to securites which a company will own after the

enforcement.

Well, from the viewpoint that a company discloses the financial

conditions as at the balance sheet date,

not as at the transaction date, to

shareholders and creditors, it may not be unreasonable to think that

one set

of financial statements should be prepared in accordance with only one

accounting standard, though.

On the accounting theory, accounting standards

should not be amended nor newly-provided at all.

For example, on the Penal Code, the base of criminal liability requires "an

objective actual act of a criminal".

In the same way, on the accounting, the

base of an accounting treatment (for examle, journal entries,

the recognition

of revenues, the accrual of expenses, the recording of assets and liabilities,

the tax base, etc.)

requires an objective actual act of a company or a

transaction of a company.

To put it simply, an accounting treatment should be

neutral to a company.

That an accounting treatment is neutral to a company

means that it is neutral to financial statements.

And, the amendment of an

accounting standard should be neutral to a transaction made before the

amendment.

Therefore, on the principle of law, as well as law,

neither the

change of an accounting treatment method in accordance with the new (amended)

accounting standard

nor the retroactive accounting treatment should not be

made.

An accounting treatment, including the initial journal entry and a

series of the following journal entiries on a transaction

is determined only

by the transaction itself as at the transaction date.

A transaction of a

company is an objective actual act of a company.

The maxim "Condemn the

offense, but not the offender." may have various meanings,

but I interpret

this maxim as "See the act only." or "Judge only by the crime itself."

If I

am right, an accounting treatment is also determined

only by a transaction

and the accounting standards as at the transaction date.

Can the amendment of

an accounting standard amend a transaction of a company?

{kind=link}

{kind=link}

{kind=link}