2015年11月21日(土)

【コメント】

深夜におやつや夜食等を買いに行くとして、家の近所の24時間開いているスーパーとコンビニのどちらに行くかと言えば、

個人的にはスーパーの方に行くと思います。

品揃えが根本的に異なるわけですから。

丸和小倉店はコンビニとの競争に負けたというより、今後は昼間の営業をさらに強化していこうという考えなのだと思います。

2015年11月21日(土)日本経済新聞

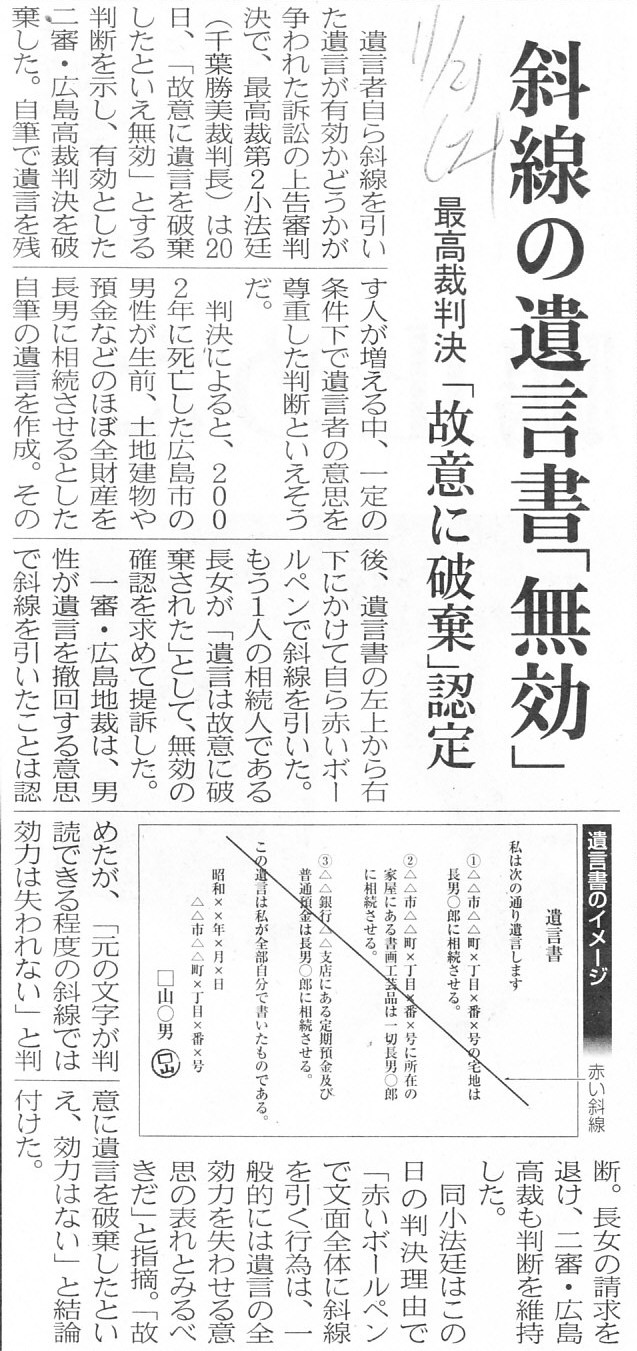

斜線の遺言書「無効」 最高裁判決 「故意に破棄」認定

(記事)

【コメント】

斜線が引かれた遺言書は無効だそうです。

では、右上に「丸印」が書かれた遺言書は有効でしょうかそれとも無効でしょうか。

答えはないでしょう。

Can you ask the deceased what that riddle means?

死んだ人に「この不可解なものはどんな意味ですか」と聞くことができますか。

【コメント】

I understand that the rationality of holding shares is

particularly an issue these days,

but, then how about a holding

company?

And, how about holding inventories?

how about fixed holding

assets?

And, ultimately speaking, how about holding cash?

保有株式の合理性が今日特に問題になっていると聞いておりますが、

では持株会社の場合はどうなるでしょうか。

また、保有棚卸資産はどうでしょうか。

保有固定資産はどうでしょうか。

そして、究極的なことを言えば、保有現金はどうでしょうか。

2015年11月20日

株式会社電通

電通、監査役会設置会社から監査等委員会設置会社へと移行

―

新たに「コーポレート・ガバナンス・ポリシー」および「社外取締役の独立性基準」を制定

―

ttp://www.dentsu.co.jp/news/release/2015/1120-008487.html

2015年11月21日(土)日本経済新聞

取締役会運営を見直し トヨカネツ

(記事)

【コメント】

Who operates a "board of directors", directors or others?

誰が取締役会を運営しているのですか。

取締役ですか、それとも、他の人たちですか。

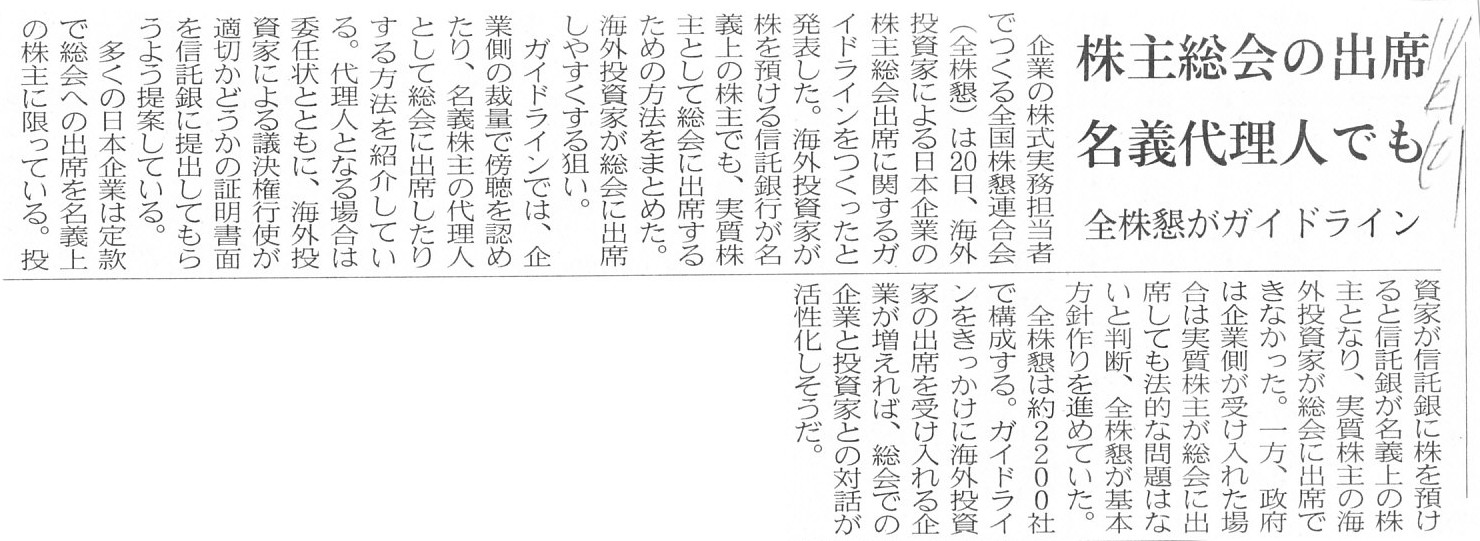

2015年11月21日(土)日本経済新聞

株主総会の出席 名義代理人でも 全株懇がガイドライン

(記事)

【コメント】

A person who is able to attend a meeting of shareholders is an

owner of a share.

株主総会に出席することができるのは、株式の所有者です。

2015年11月21日(土)日本経済新聞

新日鉄住金、海外利益ゼロ 今期経常 ブラジル苦戦、最終赤字に 鋼材市況の悪化響く

(記事)

【コメント】

More than one kinds of shares disable profits from being

distirbuted equally to respective shareholders.

株式の種類が複数あると、各株主に平等に利益を分配することができなくなります。

In other words, more than one kinds of shares disable profits from belonging equally to respective shareholders.

他の言い方をすると、株式の種類が複数あると、利益を各株主に平等に帰属させることができなくなります。

In case "all of the profits are expected tp be distributed to preferred

shares"

based on the investment contract when preferred shares were

issued,

"equity in earnings of an investee" which is recorded on a

consoilidated profit and loss statement

of a parent company in an equity

method is zero because no profits of the investee belong to the parent

company.

優先株式を発行した際の出資契約に基づき、「利益は全て優先株式に分配されることになっている」という場合、

持分法適用上の親会社の連結損益計算書に計上される「持分法投資利益」はゼロになります。

なぜなら、親会社には持分法適用関連会社の利益は全く帰属していないからです。

When the affiliate company pays a dividend only to preferred

shares,

"equity in loss of an investee" is recorded on a consoilidated profit

and loss statement

of the parent company in an equity method even though the

affiliate company records many net profits.

持分法適用関連会社が優先株式にだけ配当を支払うと、たとえ持分法適用関連会社が多額の当期純利益を計上していようとも、

「持分法投資損失」が持分法適用上の親会社の連結損益計算書に計上されます。

To conclude, the paradoxical phenomena above are not because of the wrong

interpretation on law

nor because of the wrong interpretation on

accounting.

They are purely because of the fact that more than one kinds of

shares are issued.

結論を言えば、上記の矛盾した現象は、

法律上の解釈を間違えているからでもなければ会計上の解釈を間違えているからでもありません。

純粋に、複数種類の株式を発行しているからなのです。

【コメント】

On a merger, which range of rights and obligations of an

absopted company are succeeded to a surviving company?

合併において、消滅会社の権利義務のうち、存続会社に承継されるのはどの範囲か。

Both "rights and obligations" and "assets and liabilities" are able to be

succeeded,

but, neither "profits" nor "losses" are able to be

succeeded.

「権利義務」や「資産負債」はどちらも承継させることができます。

しかし、「利益」や「損失」はどちらも承継させることができません。

Then, from a standpoint of the tax theory,

neither "incomes" nor

"neagative incomes" in the prior periods are able to be succeeded.

このことを税務理論の観点から言えば、

過年度の「所得額」や「負の所得額」はどちらも承継させることはできない、となります。

Base on the basic priciple above, "retained earnings" on the corporate

accounting are not able to be succeeded,

and "loss carryforward" on the

Corporation Tax Act are not able to be succeeded, eiher.

上記の基本原理に基づけば、企業会計上の「利益剰余金」は承継させることはできませんし、

法人税法上の「繰越欠損金」も承継させることはできない、ということになります。

{kind=link}

{kind=link}

{kind=link}

{kind=link}