2015�N10��19��(��)

2015�N10��19��(��)���{�o�ϐV���@���{�L��

���悢��A�}�C�i���o�[���������͂����܂��B

12���̃}�C�i���o�[���L�ڂ��ꂽ�w�ʒm�J�[�h�x���A�Z���[�̏Z���ɊȈՏ����ł��͂����܂��B

�w�ʒm�J�[�h�x��10��20�����`�T��11�����ɓ͂��܂��̂ŁA��ɕۊǂ��Ă��������B

���t���[�@���t�{�@����l���ی�ψ���@����Ғ��@�����ȁ@���Œ��@�����J����

�u�L��1�v

�u�L��2�v

I saw the two girls as if they were my pretty little sisters.

I wanted a

little sister then.

When I was in the eighth grade, I had a junior in school

for the first time.

I was happy to have a girl junior in school,

so I

think that I wanted to make myself so that I looked attractive as a senior in

school.

���͔ޏ�����2�l�̂��Ƃ������̂��킢�����ł��邩�̂悤�Ɍ��Ă��܂����B

���͂��̂��떅���~���������̂ł��B

���w2�N���ɂȂ��āA��y�����߂Ăł��܂����B

���̌�y���ł��Ă��ꂵ�������̂ł��B

����ŁA1�l�̐�y�Ƃ��Ċi�D�����������̂��Ǝv���܂��B

2015�N10��19��(��)���{�o�ϐV��

���I�����ɑ������������ā@��Ƃ̑����Đ��_���@��������̕ی� �ۑ�

�i�L���j

���҂ɂƂ��ẮA���K���̕����́A���҂���������ꍇ�͐Ŗ��㑹���s�Z���̔�p�ɂȂ�܂��B

�����āA���҂����Z����ꍇ�́A���҂ɂƂ��ċ��K���̕����͐Ŗ��㑹���Z���\�Ȕ�p�ɂȂ�܂��B

Whether voluntary renegotiations or legal liquidation,

creditors as at

the date of the beginning of any reorganization procedure are all as it were

"residual creditors".

For an obligor can settle arbitrary payables before a

reorganization procedure begins.

���I�����ł��낤���@�I�����ł��낤���A�ǂ�ȓ|�Y�葱���ł���A

�葱�����J�n���ꂽ�����_�̍��҂Ƃ����̂͊F�A����u�c���ꂽ���ҁv�Ȃ̂ł��B

�Ƃ����̂́A���҂͓|�Y�葱�����J�n�����O�ɔC�ӂɋ��K����ٍςł��邩��ł��B

��U�c��������~���ꂽ�Ȃ�A�c�����͂��̌��x�ƕ����͂��܂���B

���̌��t�̈Ӗ��́A��U��Ђ����炩�̓|�Y�@��K�p���ꂽ�Ȃ�A���Ȃ킿�A��U��Ђ��@�I�ȓ|�Y�葱���ɓ������Ȃ�A

���̉�Ђ͐��Z���邵���Ȃ��A�Ƃ����Ӗ��ł��B

If a company wants to avoid its liquidation, the company can't help

making private negotiations with creditors.

���Z����������̂Ȃ�A��Ђ͎��I���������邵���Ȃ��Ƃ������Ƃł��B

The original meaning of "seiri" (It is Japanese.) in this context means

"liquidation", I suppose.

���̕����ɂ�����u�����v�Ƃ������{��̌��X�̈Ӗ��́A�u���Z�v�Ƃ����Ӗ��Ȃ̂��Ǝv���܂��B

Of course, it can occur that a company is liquidated as the result of

private negotiations with creditors.

�������A���I�����̌��ʁA��Ђ����Z����邱�Ƃ͂���܂��B

In short, it can never occur that a company is not liquidated as the

result of legal bankruptcy proceedings.

�v����ɁA�@�I�����̌��ʁA��Ђ����Z����Ȃ����Ƃ͂��蓾�Ȃ��Ƃ������Ƃł��B

In case the residual assets are left in a company, after all of the

liabilities are settled in the proceedings,

all of the residual assets are

distributed to shareholders and the company is liquidated.

For shareholders

have already been creditors of the company.

An obligation which the creditor

who formerly was one of the shareholders has is a vested obligation.

This

means that the creditor is the legally vested creditor and that he will not be a

shareholder again.

The only two differences between the obligation which he

has and the obligation which the other creditors have is

the order of the

settlement and the amount of the obligation.

For him, the order of the

settlement is the last.

And, the amount of the obligation has not been

finalized yet

because it will be finalized after all of the other liabilities

are settled.

In this point, the obligation is an extremely special vested

obligation.

The cash which he receives as the distribution of the residual

assets is a taxable income totally,

but at the same time, the loss on the

write-off of the share is tax deductible.

So, only the difference between the

amount of the cash and the book value of the share

is either a taxable income

or tax deductible.

������A�@�I�����ɂ����āA�S�Ă̍���ٍς�����A��ЂɎc�]���Y���c���Ă���ꍇ�́A

�S�Ă̎c�]���Y�͊���ɕ��z���Ă��܂��A��Ђ͐��Z���邱�ƂɂȂ�܂��B

�Ȃ��Ȃ�A����͊��ɉ�Ђ̍��҂ƂȂ��Ă��邩��ł��B

���Ă͊����1�l�ł��������҂������Ă�����Ƃ����̂́A�m����ɂȂ�܂��B

���̂��Ƃ́A���̍��҂͖@���I�Ɋm�肵�����҂ł���Ƃ����Ӗ��ł����āA

���̌�Ăъ���ɂȂ�Ƃ������Ƃ͂Ȃ��Ƃ����Ӗ��ł��B

������ł�����҂������Ă���ƁA���̍��҂������Ă�����Ƃ̈Ⴂ�́A�ٍς̏��ʂƍ��̋��z��2�����ł��B

������ł�����҂ɂƂ��ẮA�ٍς̏��ʂ͈�ԍŌ�ɂȂ�܂��B

�����āA���̋��z�͂܂��m�肵�Ă��܂���B

�Ȃ��Ȃ�A������ł�����҂ɂƂ��Ă̍��̋��z�́A���̑S�Ă̍����ٍς��ꂽ��Ɋm�肷�邩��ł��B

���̓_�ɂ����āA������ł�����҂������Ă���Ƃ����̂́A�ɂ߂ē���Ȋm����Ȃ̂ł��B

������ł�����҂��c�]���Y�̕��z�Ƃ��Ď�錻���́A�S�z���Ŗ���v���ƂȂ�܂����A

�����ɁA���L�����̏��p�Ɋւ��鑹�����Ŗ��㑹���ɂȂ�܂��B

���������āA����������z�Ə��L�����̒��뉿�z�Ƃ̍��z�݂̂��A�Ŗ���̉v�����Ŗ���̑������̂ǂ��炩�ƂȂ�܂��B

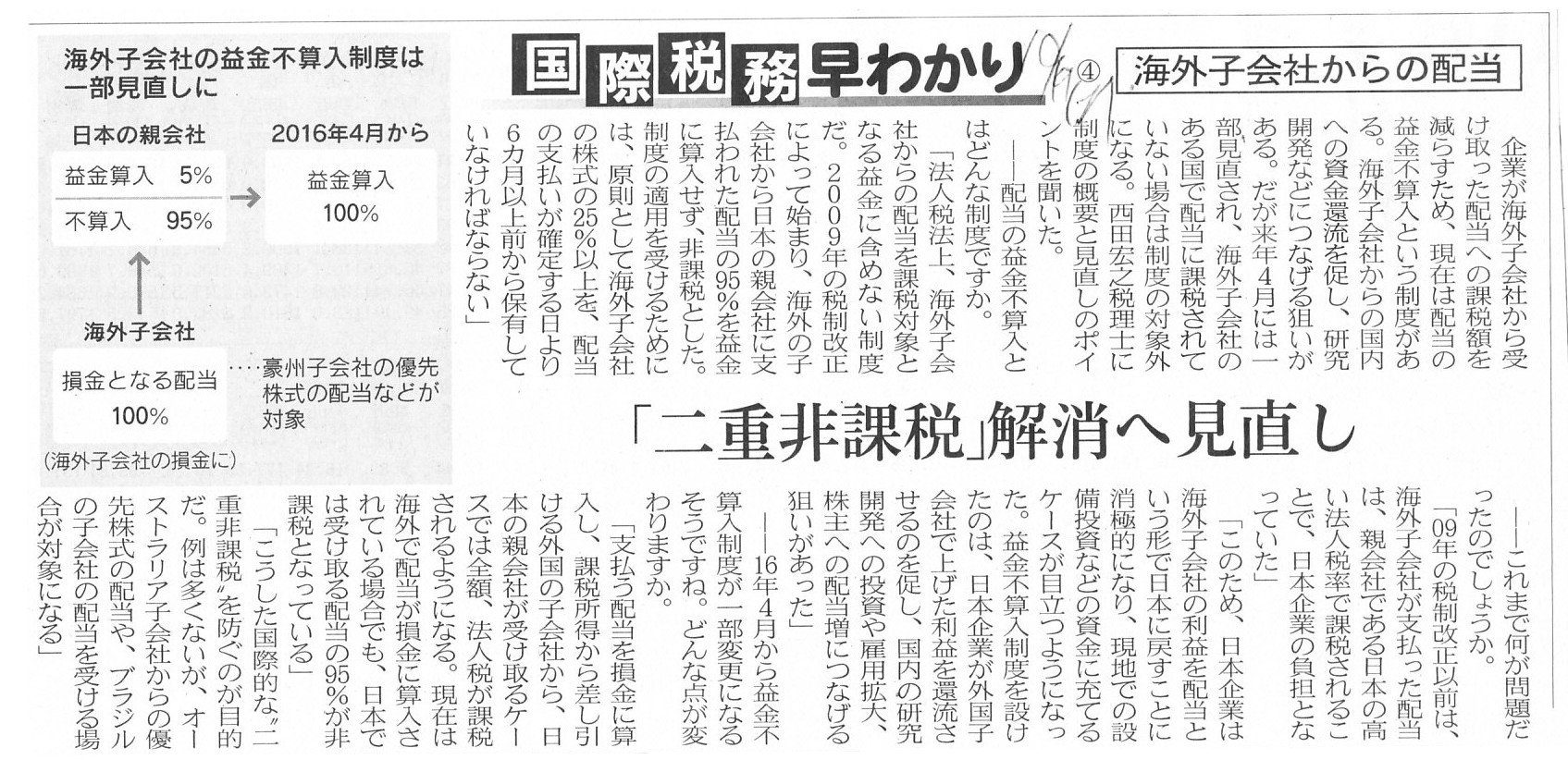

2015�N10��19��(��)���{�o�ϐV��

���ۉېő��킩��@�C�@�C�O�q��Ђ���̔z��

�u��d��ېŁv����������

�i�L���j

�y�R�����g�z

There exists neither the "double taxation" nor the "double

non-taxation".

�u��d�ېŁv���Ȃ���u��d��ېŁv������܂���B

�@�l�Ŗ@�̊ϓ_���猾���A��Ђ��s�����v�̕��z�͊�t�̈��ł���ƒ�`�����̂ł��B

������A���̑�����͊���݂̂ł���A���̍����͗��v��]���݂̂ł���A�Ƃ�����t�ł��B

��Ђ́A����ȊO�̐l�֔z�����x�������Ƃ͂ł��܂���B

��t�̍����͗��v��]���݂̂ł���Ƃ������Ƃ́A

��Ђ͗��v��]�����}�C�i�X�ł��鎞�͔z�����x�������Ƃ��ł��Ȃ��A�Ƃ����Ӗ��ł��B

�u�z���͑��v�v�Z���Ɍv�コ��Ȃ��B�v�Ƃ������t�͂��������Ӗ��Ȃ̂ł��B

��Ђ��s�����v�̕��z�Ƃ����̂́A�����������������������ۂ��ꂽ�ɂ߂ē���Ȋ�t�̂��ƂȂ̂ł��B

�N�����A����d�v�Ȏ�����Y��Ă��܂��Ă���悤�Ɏ��͎v���܂��B

��Ђ̗��v��]���Ƃ����̂́A���͐ň�����ł��邾���łȂ��A�������������Z�����s��ꂽ��́A�ł���킯�ł��B

�ň�����ł���Ƃ������Ƃ́A�����Z�����s��ꂽ��́A�Ƃ����Ӗ��ł��B

�Ȃ��Ȃ�A�ېŏ����z�Ƃ����̂́A�S�Ẳv���ƑS�Ă̑����Ƃ̗����ɂ��Z�肳�����̂�����ł��B

�ł�����A���ɔz�����Ŗ���̑����Ƃ������ƂɂȂ�܂��ƁA

��Ђ��z���Ƃ��Ďx���������͌���u��d�T���v�Ƃ������ƂɂȂ�킯�ł��B

�v����ɁA��Ђ̗��v�Ɣ�p�Ɋւ���S�Ă̌v�Z�́A�u���������v�v���Z�o���ꂽ���_�Ŋ��Ɋ������Ă��܂��Ă���킯�ł��B

�u���������v�v�̌��ʂƂ��ĉ�Ђ����L���Ă��錻���Ƃ����̂́A����u���S�Ɍv�Z���I�������́v�ł���킯�ł��B

���ǁA�u���������v�v�̌��ʂƂ��ĉ�Ђ����L���Ă��錻�������̌㑹���Z������邱�ƂɂȂ�̂������s�Z���Ƃ������ƂɂȂ�̂��́A

���̎g�r�ɂ�茈�܂�A�Ƃ������ƂɂȂ�킯�ł��B

���̎g�r���I�����Y�̎d����ł���ꍇ�́A���̌����͒I�����Y���̔����ꂽ���ɑ����Z������܂��B

���̎g�r���Œ莑�Y�̎擾�ł���ꍇ�́A���̌����͌������p�葱����ʂ��đ����Z������܂��B

���̎g�r�����̐l�ւ̊�t�ł���ꍇ�́A���̌����͌����đ����Z������܂���B

���̎g�r������ւ̊�t�ł���ꍇ���A���Ȃ킿�A���̎g�r���z���ł���ꍇ���A���̌����͌����đ����Z�������ׂ��ł͂���܂���B

��t��z���������Z��������ʂƂ����̂��S���Ȃ��킯�ł��B

�u���������v�v�̌��ʂƂ��ĉ�Ђ����L���Ă��錻���Ƃ����̂́A�����ɁA��Ђ����L���Ă���S����Ђ����̌����Ȃ̂ł��B

���̓_�ɂ����āA�u���������v�v�̌��ʂƂ��ĉ�Ђ����L���Ă��錻���Ƃ����̂́A

���{���̑�����Ƃ��Ă̌����ƁA���Ȃ킿�A���傪��Ђɕ����������ƁA���S�ɓ����ł���킯�ł��B

�ǂ���̌������A��Г��ł݂͌��ɋ�ʂ͂���܂���B

�����Ă���䂦�ɁA�ǂ���̌������A�ݎؑΏƕ\��͓����u�����v�Ƃ�������Ȗږ��Ōv�コ���̂ł��B

�u���̂����͕������܂ꂽ�����ł����A����Ƃ��A�҂��������ł����H�v�Ƃ͒N���q�˂Ȃ��̂ł��B

���_�������A��ЂɂƂ��āA�z���ɂ́u�����Z�������v�Ƃ����T�O�͂Ȃ��̂ł��B

{kind=link}

{kind=link}