2015年8月10日(月)

2015年8月10日(月)日本経済新聞

利払いの税優遇縮小 多国籍企業の税逃れ防ぐ 政府、法改正へ

(記事)

2015年8月10日(月)日本経済新聞

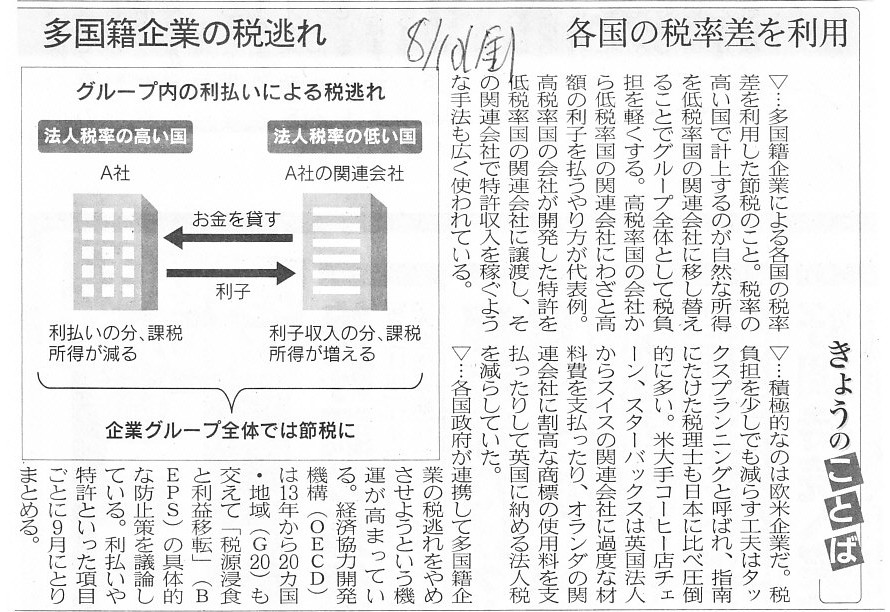

きょうのことば 多国籍企業の税逃れ

各国の税率差を利用

(記事)

【コメント】

記事によりますと、

>現行法は利払い費について所得の5割まで税務上の費用(損金)に認めているが、

>経済協力開発機構(OECD)が検討中の勧告に沿って3割までに引き下げる。

と書かれています。

現行税法の詳しい定めは見ていませんが、ここで言う税務上の”所得”とは、大まかに言えば、

「総益金−(総損金−支払利息)」

のことではないかと思います。

つまり、支払利息を税務上損金算入できるのは、総益金の5割、ではないのではないでしょうか。

記事からだけではどちらなのかは判然としませんが。

現行の法人税法を見てみますと、例えば第六十八条(所得税額の控除)にそれらしいことが書かれていますが、

損金算入は所得の5割までというようなことは何も書かれていません。

何か別の政令を見なければならないのかもしれませんが。

いずれにせよ、ある細目の損金算入可能額は所得の何割まで、という考え方は間違いだと思います。

何が損金で何が損金でないかは、その費用の特徴・性質により一意に決まる話であるはずです。

他の言い方をすれば、ある費用項目が損金として認められるかどうかは、オール・オア・ナッシングであるわけです。

費用の金額の何割、というような線引きの仕方はないはずです。

細かいことを言い出せばキリがありません。

今日は益金や損金や所得の定義だけをインターネット上の記事から引用し、

明日改めて書きたいと思います。

益金【名詞】

1 gain

企業の売り上げが運用コストを上回るときの差額

(the amount by which the

revenue of a business exceeds its cost of operating)

2 profit, net profit, lucre, earnings, net income, net,

profits

ある一定の期間内で出費を超える収益の超過部分(減価償却と他の非現金出費を含む)

(the excess of revenues

over outlays in a given period of time (including depreciation and other

non-cash expenses))

譲渡【動詞】

1 transfer

所有権を変えさせる

(cause to change ownership)

【まとめ】

現行税法で言う「益金」の一番の英訳は、「gross

revenues」になるのかもしれない。

ただ、税務のことを特に強調したい場合は「taxable

revenues」という言い方もあるようだ。

「損金」は「deductible expenses」。

「課税所得(額)」は「taxable

income」。

ウィキペディアで調べたところ、「総益金」は「gross income」という言い方を米国税法ではするようだ。

「gross

income」から「allowable tax deductions」を引き算すると、「taxable income」になるようだ。

(The

amount on which tax is computed, taxable income, equals gross income less

allowable tax deductions.)

総益金から総損金を引くと、課税所得となる。

Unless a person acquires some corporeal property, he is not able to sell

it.

有体物を取得しない限り、人はその有体物を売却できません。

To "transfer" means

that a person who have had ownership of some

property sells it to another person who will anew have ownership of it.

「譲渡する」とは、ある資産の所有権を持っていた人が新規にその所有権を持つことになる別の人へその資産を売却することです。

Let's think that a person receives some income from a transfer of some

property.

In this case, if he has never had ownership of the property nor he

will not have ownership of the property,

he should be regarded not to be

concerned with at least "the transfer of the property" itself.

This

relationship between a transfer and the income means that, to put it more

precisely,

the person doesn't receive any incomes from a transfer of some

property, actually.

ある人が資産の譲渡から所得を得たと考えてみましょう。

この時、その人が、その資産の所有権を持ちもしていないしこれから持つこともしない場合、

その人のことは少なくとも「その資産の譲渡」そのものとは何の関係もないと考えなければなりません。

このような譲渡と所得の関係というのは、より正確に言うならば、

その人は実際には資産の譲渡からは何の所得も得ていない、ということなのです。

{kind=link}

{kind=link}