2015年6月12日(金)

2015年6月12日(金)日本経済新聞 公告

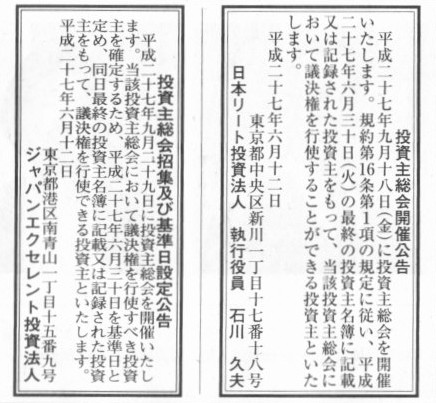

投資主総会開催公告

日本リート投資法人

投資主総会招集及び基準日設定公告

ジャパンエクセレント投資法人

(記事)

2015年6月12日(金)日本経済新聞

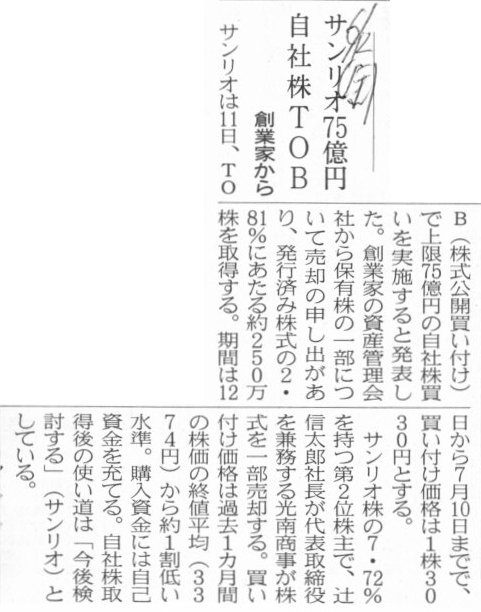

サンリオ75億円 自社株TOB 創業家から

(記事)

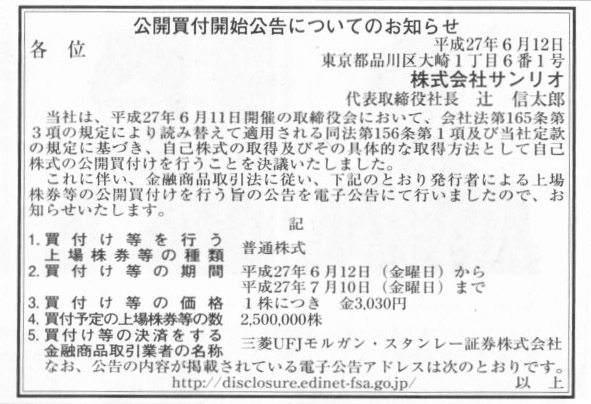

2015年6月12日(金)日本経済新聞 公告

公開買付開始公告についてのお知らせ

株式会社サンリオ

(記事)

2015年6月12日(金)日本経済新聞

セブン&アイ1200億円調達 普通社債3本

(記事)

2015年6月12日(金)日本経済新聞

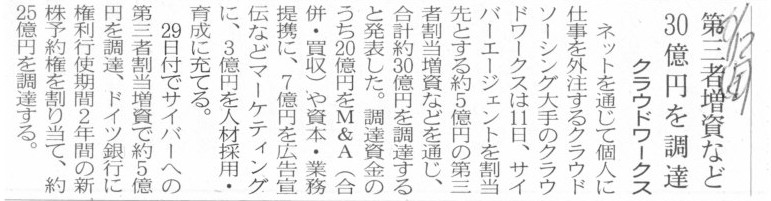

第三者増資など 30億円を調達 クラウドサービス

(記事)

2015年6月12日(金)日本経済新聞

ハイブリッド債2000億円 三菱商、当初予定の2倍

(記事)

条件というのは全てその元本に帰属しているのです。

元本が同じなままなら条件変更などは行えないのです。

つまり、条件を変更したいなら元本自体を変更しなければならない、ということです。

Conceptually speaking, when you change even one of the terms, the account

title should be changed.

It's a wrong idea that the account title don't need

changing as long as the book value is all the same.

概念的に言えば、条件を1つでも変更すれば、その勘定科目名も変更しなければならない、ということになります。

帳簿価額が同じなままなのであれば勘定科目名を変更する必要はない、と考えるのは間違いです。

An account title contains the amount, the date, the counter party and the terms.

勘定科目名には、金額、日付、取引の相手方、そして取引条件が含まれるのです。

An account title can't be renamed.

勘定科目名は、名称変更などできないのです。

A superfial transfer from the existing account to a new account is also not admitted.

表面的に旧勘定から新勘定へ振り替えることもまた認められません。

The ultimate of ultimates is that each account always has a cash account as a counter account in a journal entry.

究極中の究極のことを言えば、仕訳において全ての勘定科目の相手方勘定科目は常に現金勘定なのです。

A journal entry is not a superfial note.

飾りじゃないのよ仕訳は。

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}