2015年4月19日(日)

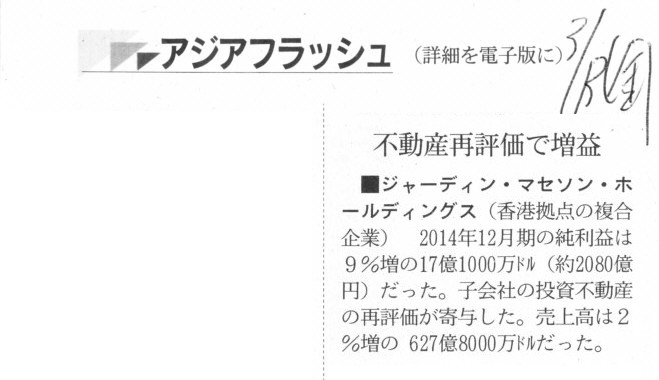

2015年3月13日(金)日本経済新聞

■ジャーディン・マセソン・ホールディングス(香港拠点の複合企業) 不動産再評価で増益

(記事)

5th March 2015

Jardine Matheson Holdings Limited

Jardine Matheson

Holdings Limited 2014 Preliminary Announcement of Results

(Unaudited)

ttp://www.jardines.com/assets/files/NewsAndEvents/corporate-press-releases/jardine-matheson/results14.pdf

>子会社の投資不動産の再評価が寄与した。

と書かれています。

2015年3月5日にジャーディン・マセソン・ホールディングスが発表した「決算短信」("immediate

release")

「Jardine Matheson Holdings Limited 2014 Preliminary Announcement of

Results

(Unaudited)」から、

「投資不動産の再評価」に関連する部分をキャプチャー・翻訳し、コメントをしてみたいと思います。

まず、「投資不動産の再評価」は当期純利益を構成するのか、というそもそもの疑問があります。

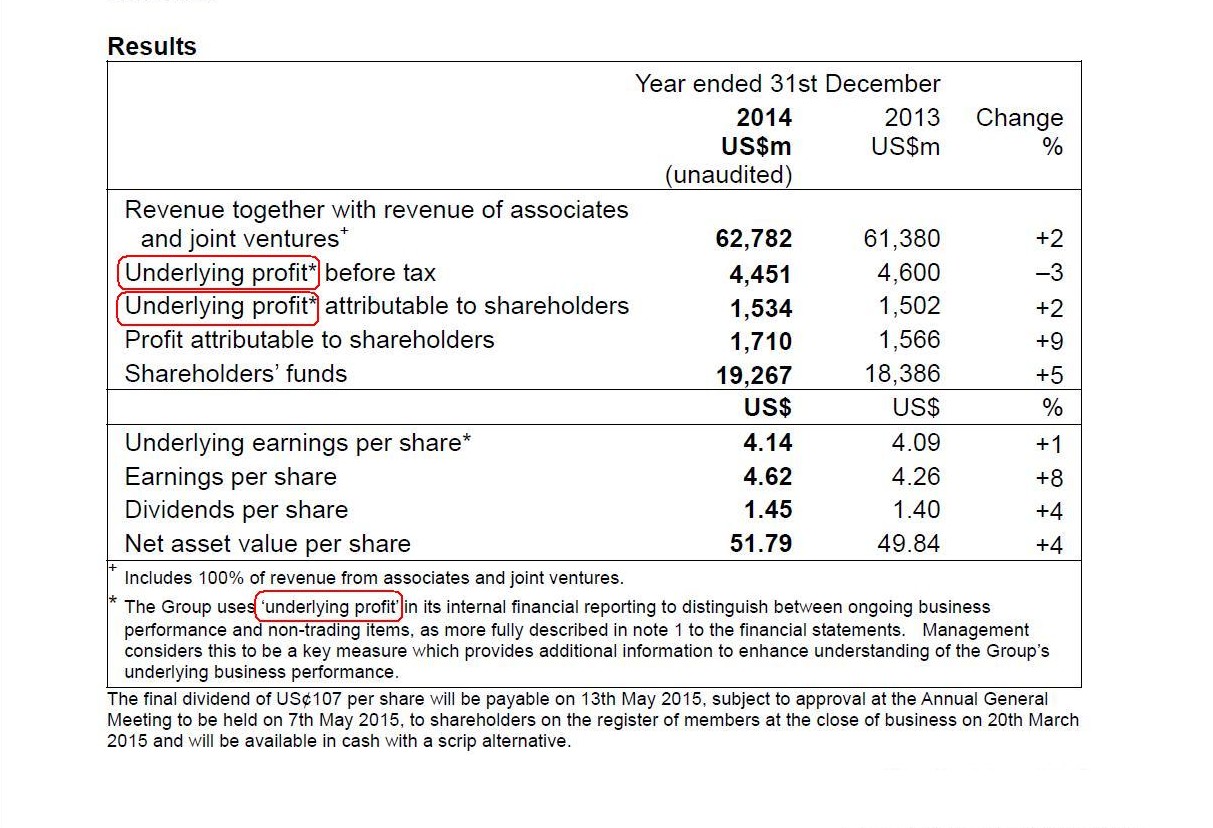

「決算短信」の1ページ目には、簡略な損益計算書が記載されており、そこに簡単な注記が書かれていますので見てみましょう。

Results

(1/33ページ)

>The

Group uses ‘underlying profit’ in its internal financial reporting to

distinguish between ongoing business

>performance and non-trading items,

as more fully described in note 1 to the financial statements.

>Management

considers this to be a key measure which provides additional

information

>to enhance understanding of the Group’s underlying business

performance.

【参謀訳】

弊社では、継続事業の業績と非営業項目とを区分するために、

社内財務報告において「基礎的利益」(underlying

profit)という言葉を用いています。

詳しい説明はこの財務諸表の注記1に記述を行っています。

弊社経営陣は、この「基礎的利益」のことを、

弊社の基礎的な事業の業績を深く理解するための情報をさらに提供する重要な判断指標だと考えています。

「投資不動産の再評価」を考える際には、この「underlying profit」という考え方がポイントとなるようです。

この「underlying

profit」とは、簡単に言えば、いわゆる「資産の評価替え」のことのようです。

所有している資産の価額を、より公正であると経営陣が考える価額へと変更することを指しているようです。

この資産の評価替えに伴い生じた資産の増加額のことを「underlying

profit」と呼んでいるようです。

決算短信を読んでいますと、

「the valuation of investment

properties」(投資不動産の評価)に関して「a net

gain」(純利益)、

という言い方をしている部分があります。

この「資産の評価替え」は、税務上の益金という取り扱いになっているようです。

そして、「資産の評価替え」による税引後の利益は、株主に帰属している、という考え方・取り扱いになっているようです。

該当部分をキャプチャーし訳してみます↓。

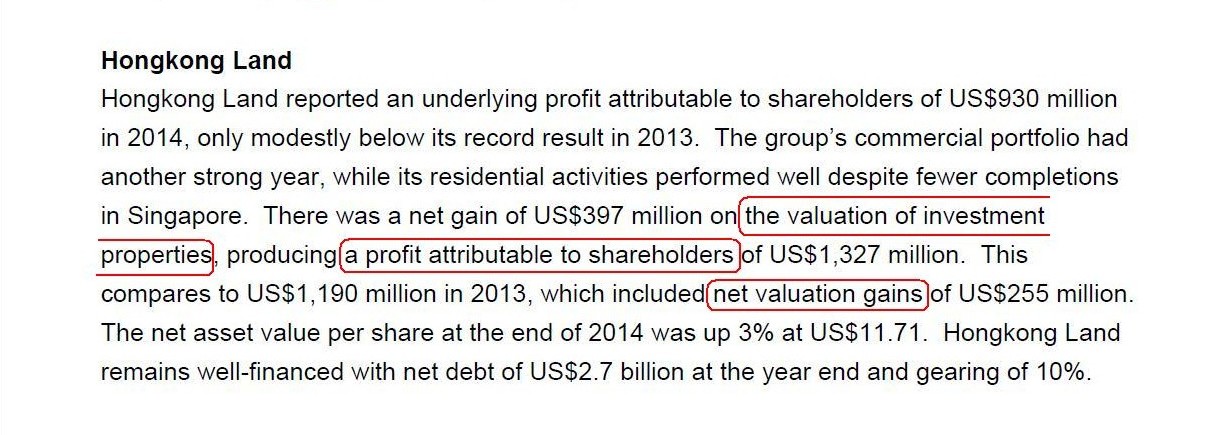

Hongkong Land

(9/33ページ)

>Hongkong

Land reported an underlying profit attributable to shareholders of US$930

million in 2014,

>only modestly below its record result in 2013. The

group’s commercial portfolio had another strong year,

>while its

residential activities performed well despite fewer completions in

Singapore.

>There was a net gain of US$397 million on the valuation of

investment properties,

>producing a profit attributable to shareholders of

US$1,327 million.

>This compares to US$1,190 million in 2013, which

included net valuation gains of US$255 million.

>The net asset value per

share at the end of 2014 was up 3% at US$11.71.

>Hongkong Land remains

well-financed with net debt of US$2.7 billion at the year end and gearing of

10%.

【参謀訳】

香港不動産は、2014年度、株主に帰属している基礎的利益は9億3000万米ドルとなったと報告しました。

これは、2013年度に記録した業績をわずかに下回るに過ぎません。

弊社の事業ポートフォリオは2014年度も力強い一年となったわけですが、

シンガポールでは完成数は減少したものの、弊社の住宅事業は立派な業績を達成いたしました。

投資不動産の評価では3億9700万米ドルの純利益を達成し、その結果、

株主に帰属している13億2700万米ドルもの利益額を生み出しました。

これは2013年度の11億9000万米ドルに匹敵します。これには2億5500万米ドルの純評価益を含んでいます。

2014年度の期末日において、1株当たりの純資産の価額は、3%増加し11.71米ドルとなりました。

香港不動産は、十分に資金調達を行っている状態にあり、

2014年度の期末日時点で27億米ドルの純負債を有し、負債比率は10%となってます。

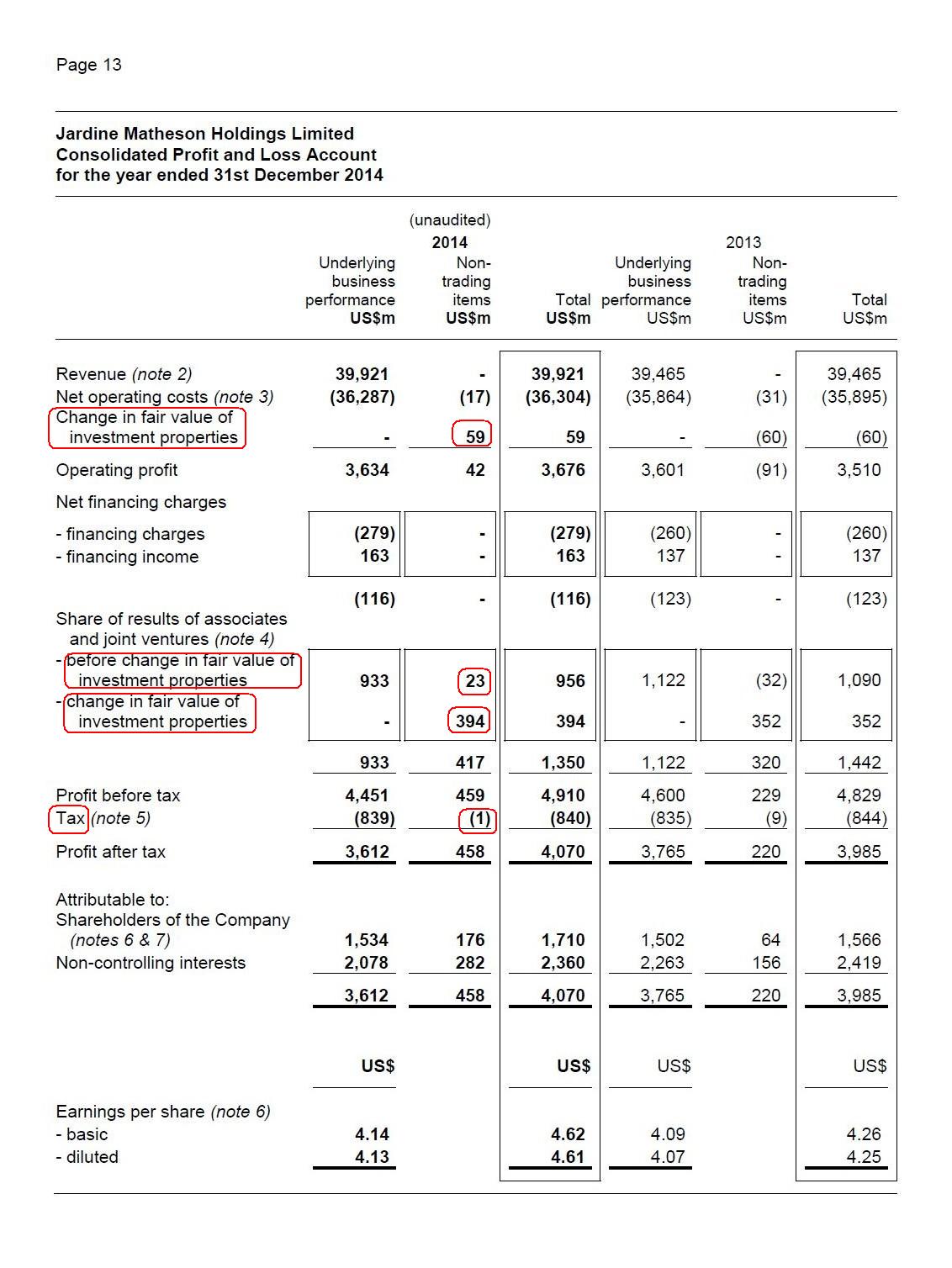

こちらは「連結損益計算書」になりますが、

「Change in fair value of investment

properties」(投資不動産の公正な価額の変更)という項目が

「Non-trading

items」(非営業項目)の1つとして記載されています。

この「Change in fair value of investment

properties」(投資不動産の公正な価額の変更)は、

「Operating profit」(営業利益)を構成するようです。

また、「Share

of results of associates and joint

ventures」(関連会社やジョイント・ベンチャーの業績の持ち分)

という損益項目が連結損益計算書にはあります。

「before change

in fair value of investment properties」(投資不動産の公正な価額の変更前)と

「change in fair

value of investment

properties」(投資不動産の公正な価額の変更)に分かれています。

例えば、持分法適用関連会社所有の資産の評価替えを連結損益計算書において連結上の利益として反映させている、

ということなのかもしれません。

そして、「Non-trading

items」(非営業項目)にも「Tax」(法人税)の金額が記載されているということは、

資産の評価替えも税務上の益金という考え方なのかもしれません。

Consolidated Profit and Loss Account for the year ended 31st December

2014

(13/33ページ)

それで、結局、「基礎的利益」(underlying

profit)が何だったのかはこの決算短信を読んでもよく分かりませんでした。

「基礎的利益」(underlying

profit)と「資産の再評価」の関係について知りたかったのですが。

「Non-trading

items」(非営業項目)が「基礎的利益」(underlying profit)と関連があるはずだと思いますので、

「Non-trading

items」(非営業項目)についての注記を訳して今日は終わりたいと思います。

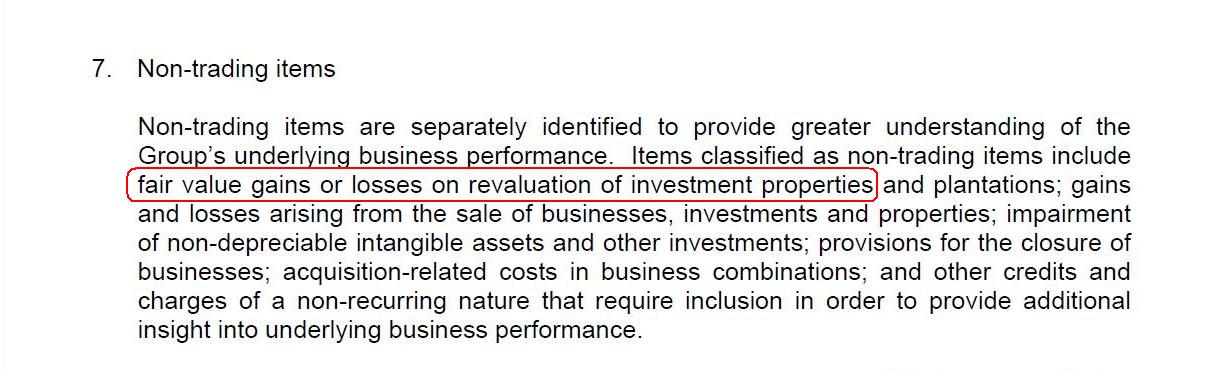

7. Non-trading items

(25/33ページ)

>Non-trading

items are separately identified to provide greater understanding of the Group’s

underlying business performance.

>Items classified as non-trading items

include fair value gains or losses

>on revaluation of investment

properties and plantations;

>gains and losses arising from the sale of

businesses, investments and properties;

>impairment of non-depreciable

intangible assets and other investments;

>provisions for the closure of

businesses;

>acquisition-related costs in business

combinations;

>and other credits and charges of a non-recurring nature

that require inclusion

>in order to provide additional insight into

underlying business performance.

【参謀訳】

非営業項目は、弊社の基礎的な事業の業績の理解に資するために、個別に認識されます。

非営業項目として分類された項目には、以下の項目が含まれます。

①投資不動産や工場設備の再評価に関する公正価値損益

②事業や投資資産や不動産の売却から生じる損益

③非減価償却の無形資産や他の投資勘定の減損

④閉鎖する事業への引当金

⑤企業結合の際の買収関連費用

⑥基礎的な事業の業績へのさらなる洞察に資するために、含めて考える必要がある非経常的な事柄に関する債権と費用

訳してみると、この「Non-trading items」(非営業項目)の説明が「基礎的利益」(underlying

profit)の説明になっているようです。

1/33ページの「note 1」(注記1)は、「note

7」(注記7)の間違いだったのかもしれません。

The meaning of the value of a land account recorded in a balance sheet.

貸借対照表に計上された土地勘定の価額の意味。

Is the revaluation of an asset a certain profit earned or just a difference of the asset?

資産の再評価というのは、稼得した何らかの利益なのですか、それとも、ただの資産の差額なのですか?

The term "believe" or "consider" troubles me. The term "is" only can save me.

「信じる」や「考える」では困ります。「これです」という言葉が必要なのです。

Ultimately speaking, what you call a profit or something of that nature such as revenues or earnings is only cash.

究極的なことを言えば、収入や所得といったいわゆる利益やそれに類するものというのは全て、現金のことなのです。

It is only a profit which has actually been realized, not a profit which is likely to be realized, that supports a company.

現に実現した利益のみが会社を支えるのです。将来そうなりそうな利益は会社を支えません。

The fair value after the acquisition is merely an opinion.

But, the fair

value at the acquisition is the fact.

The fair value is detetmined not by the

management or somebody but only by the fact of an asset's being acquired.

取得後の公正な価額というのは、意見に過ぎません。

しかし、取得時の公正な価額は、事実なのです。

公正な価額は、経営陣か誰かが決めるものではありません。

公正な価額は、資産が取得されたという事実のみによって決まるのです。

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}